Grid constraints threaten Europe’s energy security ambitions

Europe risks undermining its energy security and industrial competitiveness due to insufficient electricity grid capacity, with at least 120 GW of planned renewable projects facing delays, according to a report by Ember published on April 1.

Europe’s switch to renewables is going well. his year Spain met its entire demand for power with renewable energy at the start of April for the first time ever. Currently, Europe gets just under half of all its power from renewables.

However, last year’s Iberian Peninsula blackout was caused by large swings in renewable power generation that overloaded the grid and caused it to shut down. Gas fired power stations, by comparison, can be strictly controlled and give a much more stable output of power requiring a less robust grid. Investment has been pouring into building more generation capacity, but parallel investment into the grid has been lagging.

That is starting to turn into a bottleneck. Ember reports that across 20 EU countries, grid infrastructure is not keeping pace with the bloc’s energy transition or industrial electrification needs. Around half of reporting countries lack the capacity required to connect new renewable generation, with the most severe constraints concentrated in Austria, Bulgaria, Latvia, the Netherlands, Poland, Portugal, Romania and Slovakia.

“Grids will determine the success of Europe’s mission to wean itself off imported fuels and expand its industrial base,” said Elisabeth Cremona, senior energy analyst, Europe at Ember.

Transmission bottlenecks put majority of renewables at risk

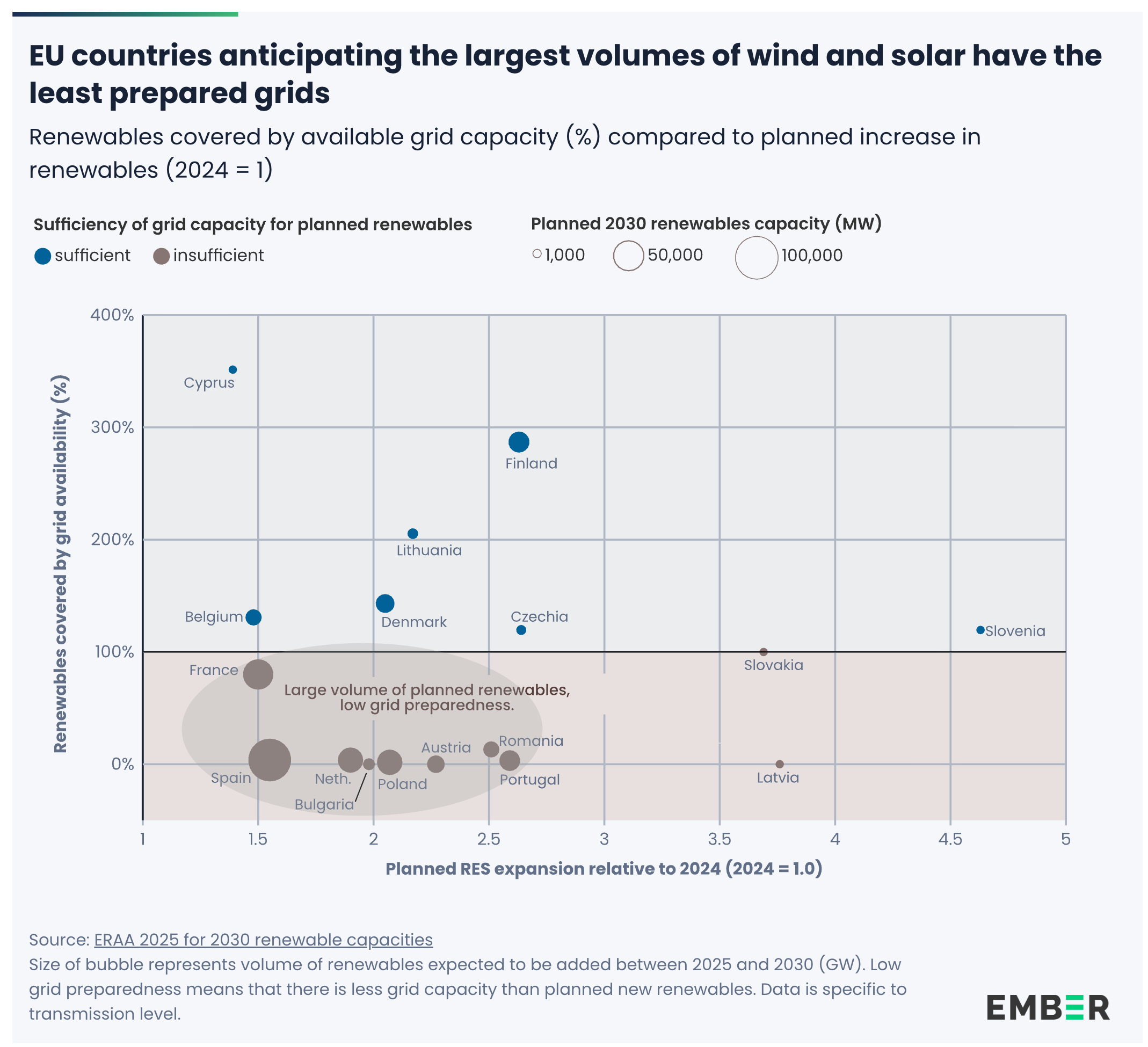

The largest constraints are found at transmission level, where large-scale wind and solar projects connect. Ember identifies a 104 GW shortfall across 17 reporting countries, with 10 already facing capacity gaps.

Of the 158 GW of renewables expected to be deployed by 2030 in these countries, as much as 66% may not materialise due to connection barriers. In several of the most constrained markets, available grid capacity can accommodate less than 10% of planned additions.

The pressure is near-term. By 2028, nine of the 17 countries are expected to face acute grid shortages, including the Netherlands, where congestion has already begun to delay projects and increase system costs.

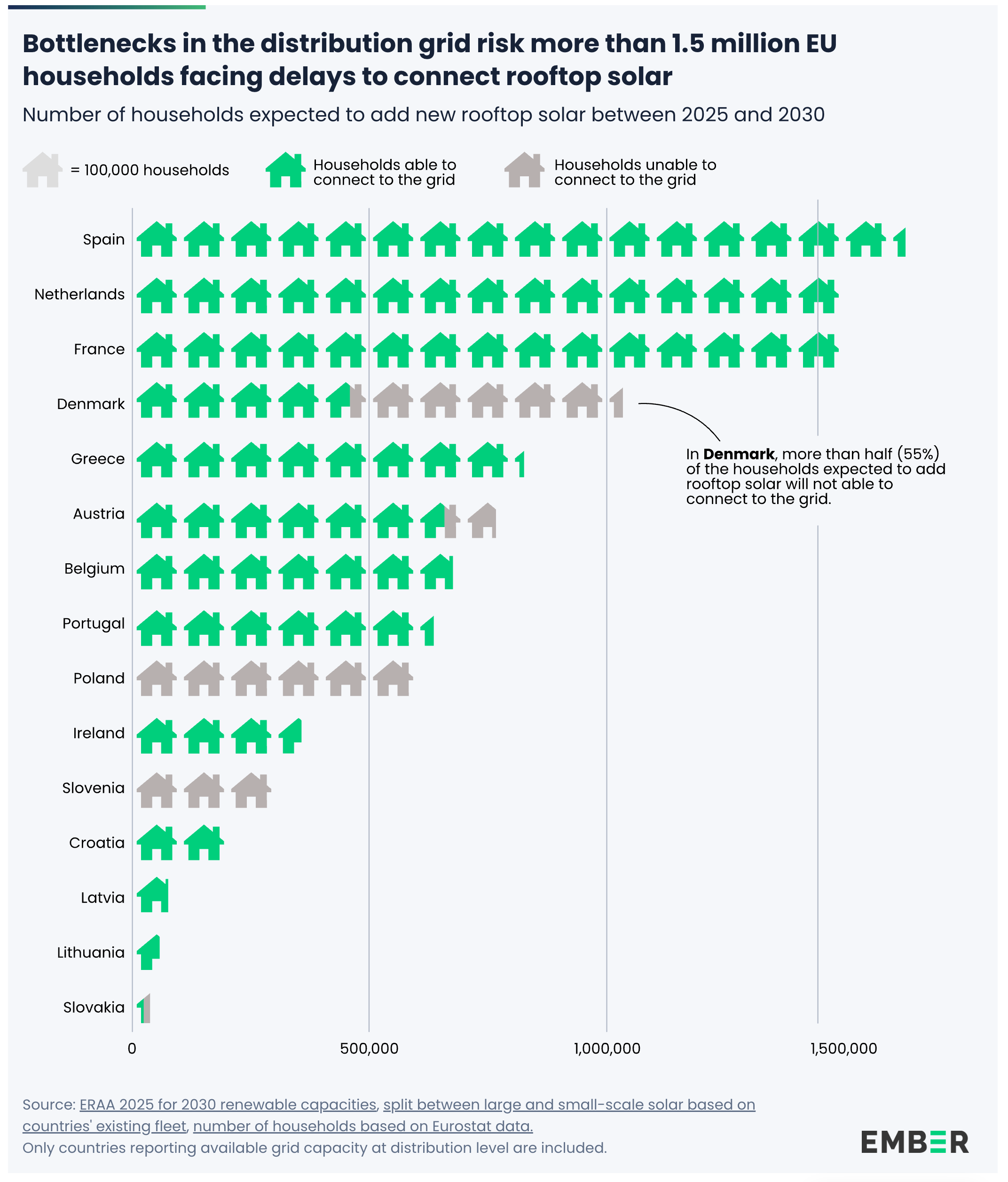

Constraints at distribution level threaten smaller-scale solar deployment too. Of 13 countries reporting data, six lack sufficient capacity to support expected growth in rooftop installations.

At least 16 GW of planned rooftop solar by 2030 is at risk, affecting up to 1.5mn households. Slovenia and Denmark are the most exposed, with grid limitations potentially impacting 32% and 19% of households respectively.

Rooftop systems currently account for 61% of the EU’s installed solar capacity, making distribution grid readiness critical for continued expansion.

Connection queues reveal scale of unmet demand

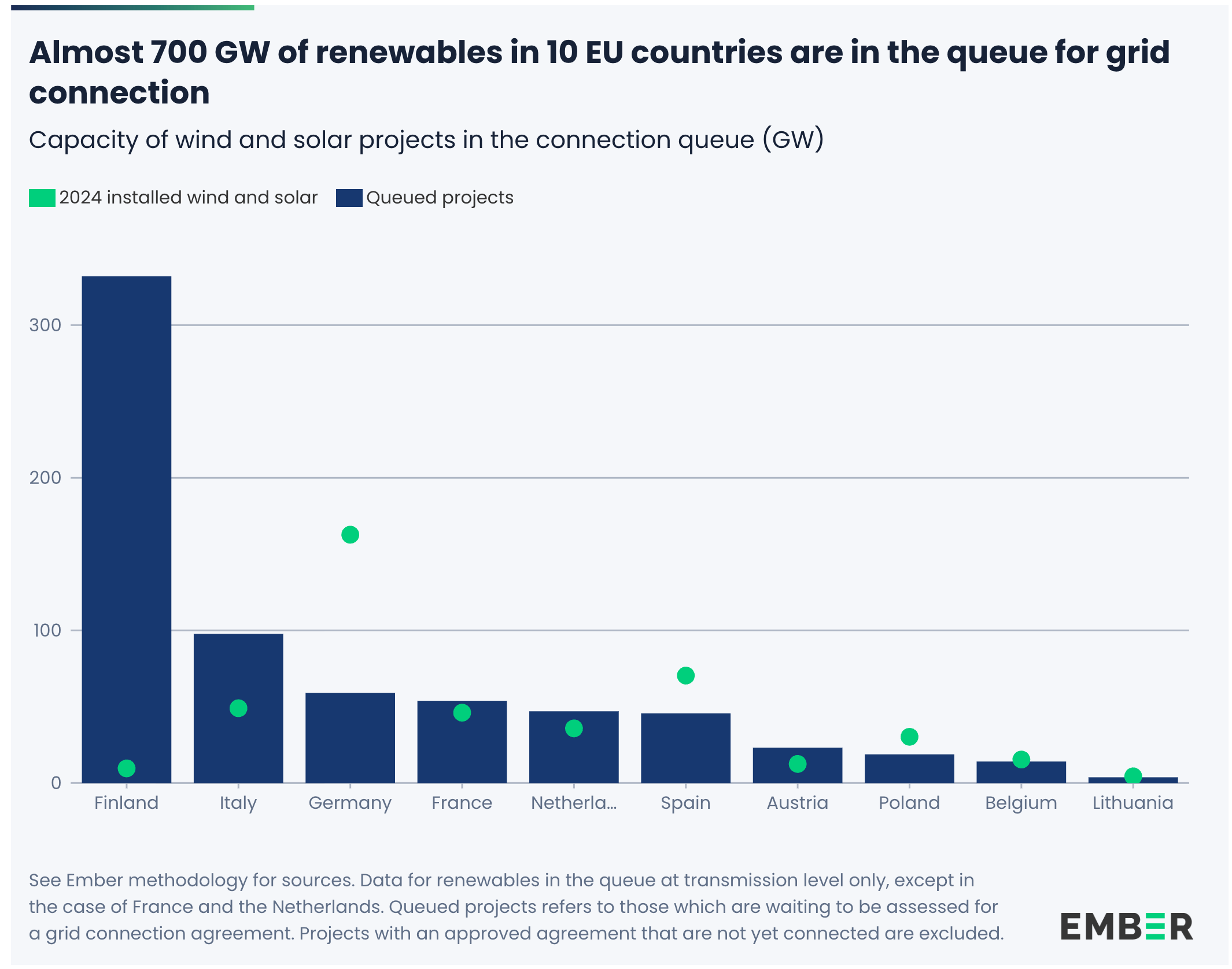

Grid congestion is compounded by a growing backlog of projects awaiting connection. Nearly 700 GW of renewable capacity is currently in connection queues across eight reporting countries.

In Finland, project inquiries exceed 400 GW, more than 16 times its existing generation capacity of 24.5 GW. While not all projects will proceed, the figures illustrate the scale of competition for limited grid access.

In Italy, 231 GW of projects have already secured connection agreements, equivalent to 169% of the country’s installed capacity, highlighting the disconnect between planning pipelines and physical infrastructure.

Grid capacity for new industrial loads varies widely. Among seven countries reporting transmission-level data, three — Austria, Bulgaria and Romania — report zero available capacity.

Czechia stands out with 6.3 GW of available capacity, equivalent to 60% of its 2024 peak demand. Belgium and Latvia also report relatively strong headroom, while the Netherlands has around 1 GW available, or 5% of peak demand.

In Denmark, a surge in applications led transmission system operator Energinet to pause new connections in March 2026. More than 60 GW of demand is now queued, compared with a national peak demand of 7.3 GW in 2024.

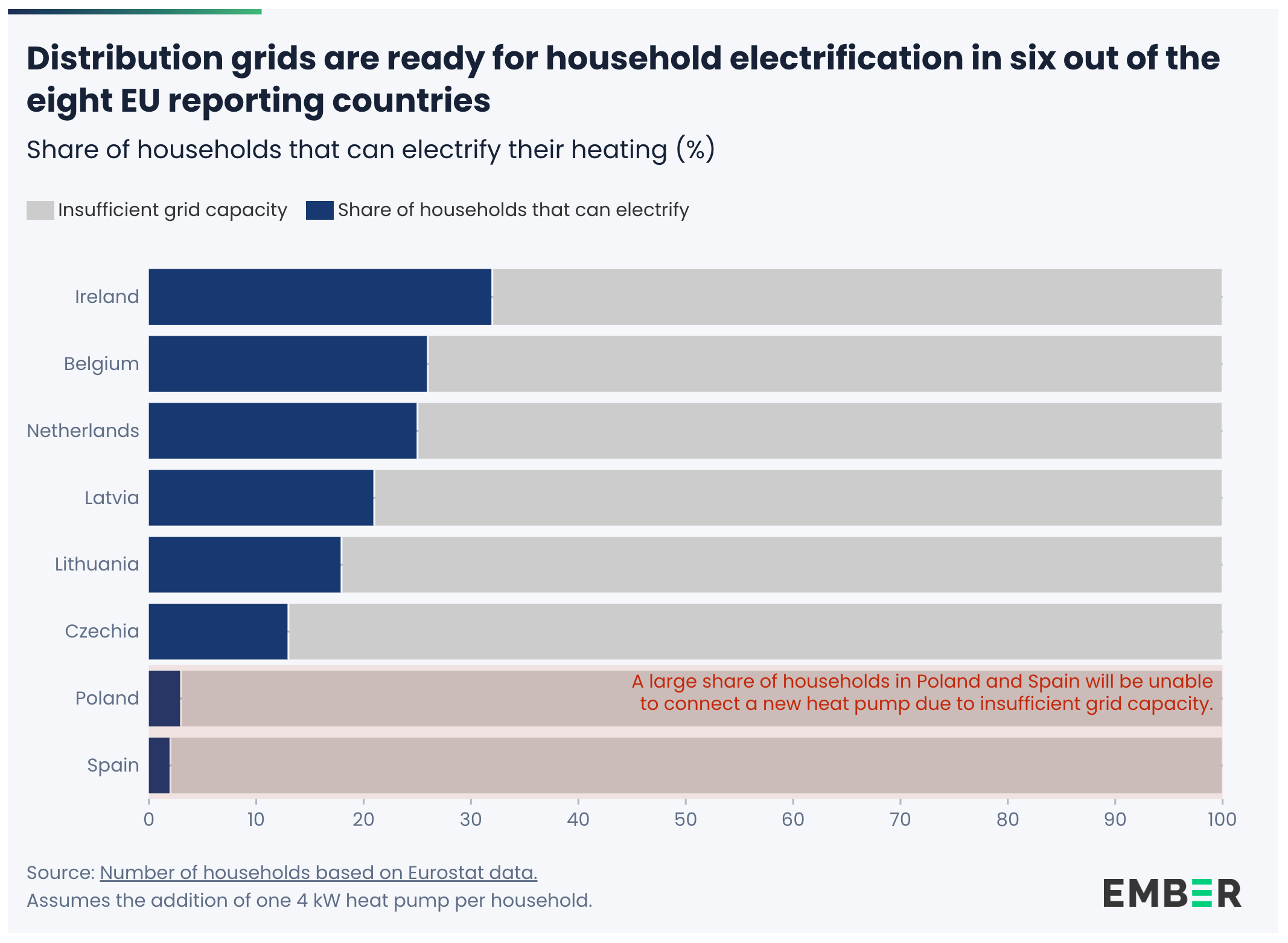

Distribution grids are comparatively better positioned to support electrification of households. Six of eight reporting countries can accommodate heat pumps in 13% to 32% of households and electric vehicle chargers in 7% to 18%.

Ireland leads, with capacity for heat pumps in 32% of households and EV chargers in 18%. Belgium and Latvia follow, with capacity for 26% and 21% of households respectively.

Spain and Poland lag significantly, with capacity sufficient for only 1% to 3% of households.

Non-wire solutions could unlock up to 185 GW

Ember highlights that non-wire solutions could rapidly alleviate constraints without requiring new infrastructure. Grid-enhancing technologies and flexible connection agreements could unlock between 140 GW and 185 GW of additional capacity.

By November 2025, 15 EU Member States had introduced frameworks for non-firm connections. In the Netherlands, transmission system operator TenneT reported that such agreements have already unlocked 9.1 GW of capacity, equivalent to 40% of national peak demand.

Targeted allocation mechanisms are also being deployed. In Spain, 99% of 200 GW of grid capacity is already reserved and allocated through tenders, while France has pre-allocated around 71 GW for renewables under regional planning schemes.

“Ambitions alone cannot move electrons,” Cremona said, warning that without rapid reform of connection processes and faster deployment of grid solutions, Europe’s energy security goals risk being delayed.

Follow us online