Russia’s oil windfall from the Iran war masks a slower decline

Russia’s oil industry has been handed a short-term reprieve by the war in Iran and the closure of the Strait of Hormuz, but the boost from triple-digit crude prices does not alter the sector’s deeper trajectory, Sergey Vakulenko, an oil analyst said in a note for Carnegie Endowment for International Peace.

Vakulenko says the immediate effect is clear: “The abrupt rise of oil prices caused by the Iran war… will bring a windfall both to the Russian oil companies and the state.” Higher prices could lift drilling spending and temporarily support output, he says, but “it would not change the long-term outlook and fundamentals of the Russian oil industry”.

His central argument is that Russian production is unlikely to collapse but is instead set for “a slow but steady production decline” that is “relatively insensitive to oil prices”. The main constraints are not geology or even technology, but “state policy, the investment climate, and OPEC+ constraints”.

The recent drop in output since late 2025 was probably not proof of a systemic breakdown. “The production decline in December 2025 through January 2026 was almost certainly driven by exceptional circumstances rather than a deep systemic crisis,” he writes, linking it to Ukrainian drone strikes on Lukoil’s Caspian offshore platforms. Even so, the episode exposed more important structural questions: at what price Russian fields remain economic, how much the state extracts, and whether companies still have the incentive to invest.

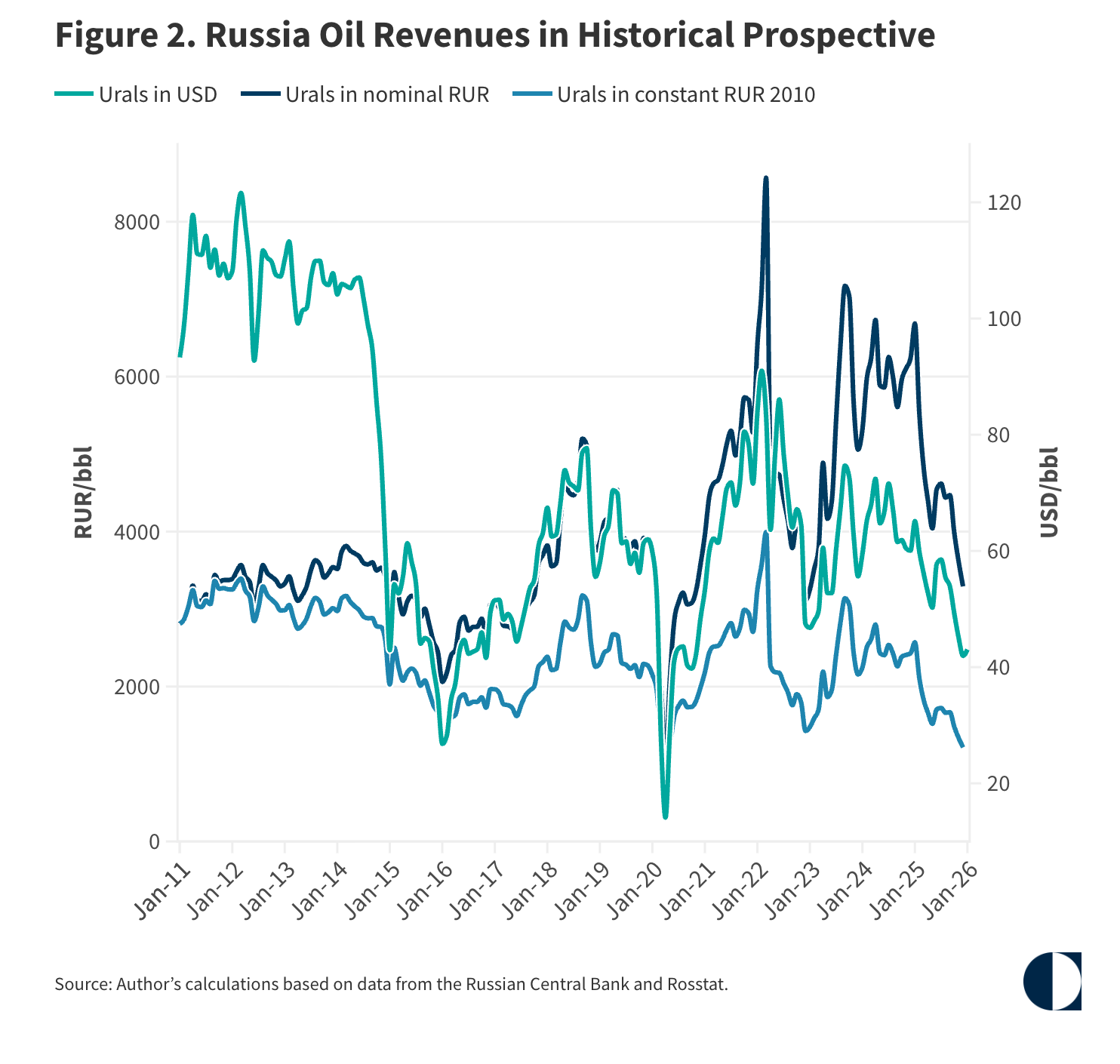

On taxation, Vakulenko says the Russian fiscal regime still reflects a long-standing state instinct to capture as much rent as possible. “The state collects 58.4% of all revenue above $13.5/bbl,” he writes. At the Urals price of $39.20 a barrel in December 2025, companies retained about $24 a barrel after tax, which he says was enough to keep production viable, though not enough to encourage aggressive expansion.

He dismisses the more extreme claims about Russian costs as misleading. The relevant threshold, he says, is not whether production stops, but whether new drilling slows. Existing output can survive even at very low prices because mature brownfield production remains cheap to run. “Production is therefore unlikely to stop; it will simply decline at its natural depletion rate as the mature well stock runs down,” he writes.

Vakulenko also argues that Russia’s technical capabilities remain stronger than many western policymakers assume. Sanctions have complicated access to capital and some specialist equipment, but they have not broken onshore operations. Russia’s industry can still deploy “technology at current global standards of practice at remarkably competitive costs”, with Chinese supply helping to fill gaps.

The bigger problem is the project pipeline. OPEC+ quotas have reduced the incentive to sanction new developments, while war, sanctions, labour shortages and high capital costs have pushed large frontier projects, especially in the Arctic, out of reach.

|

Major OPEC+ Oil Producers and Exporters |

|||

|

Country |

Year |

Production (mmbbl/d) |

Exports (mbl/d) |

|

Russia |

2025 |

9.2 |

6.5 |

|

Russia |

2030, base case |

8 |

5 |

|

Saudi Arabia |

2025 |

10.1 |

6.1 |

|

UAE |

2025 |

3.2 |

2.1 |

|

Iraq |

2025 |

4.2 |

3.3 |

|

Sources: “OPEC Monthly Oil Market Report,” Statistical Review of World Energy, March 2026, p. 64; Joint Organizations Data Initiative, International Energy Forum; and “Russia's February oil and fuel exports lowest since start of Ukraine war, IEA says,” Reuters, March 12, 2026, |

|||

“Virtually all new project development appears to be mothballed,” he writes, with Vostok Oil the only notable exception. Companies have instead relied on tighter infill drilling, a strategy that supports output now but “will produce a sharper production decline in the future”.

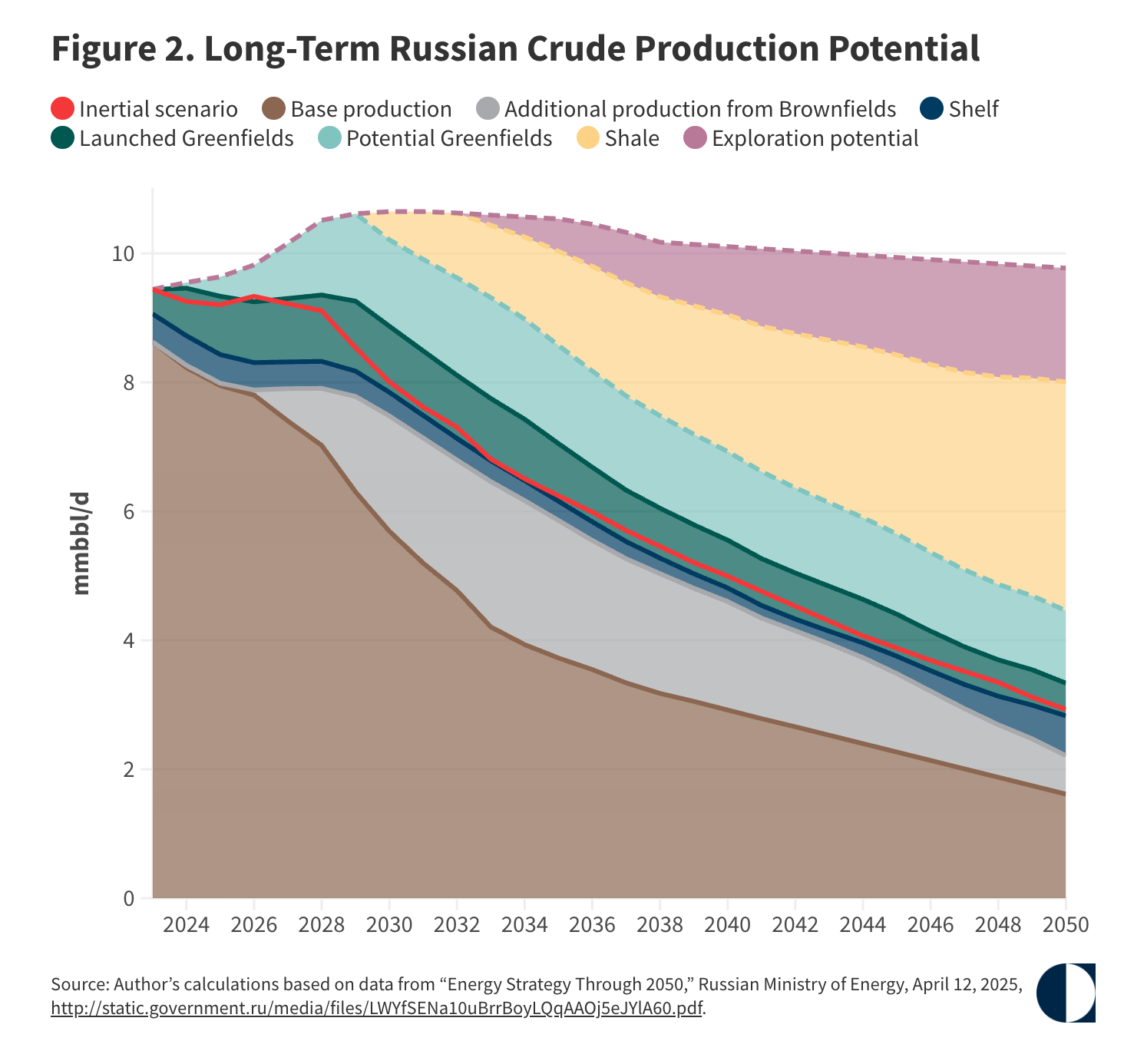

Vakulenko says Russia’s own 2050 energy strategy effectively concedes the point. The official target scenario assumes a plateau that looks politically necessary rather than commercially plausible, while the base case points to decline. “This trajectory implies output falling to approximately 8mn b/d by 2030 and below 7mn b/d by 2035,” he writes from the current 10.5mn b/d.

He describes the industry as being in “zugzwang”, forced into choices it would rather avoid. The sector can manage a decline of roughly 3% a year without much difficulty, he says, but sustaining flat output would require developing higher-cost resources that need more capital and more generous fiscal terms than the state is prepared to allow.

“The Russian oil industry currently lacks the capital to do so, and the state lacks the willingness to leave that capital in the industry’s hands,” he writes.

That leaves room for alternative outcomes, but only under demanding conditions. Vakulenko says production growth would require companies to retain “at least $45/bbl after taxes” from new barrels, reform of quota allocation, an end to the war in Ukraine, looser sanctions and broader access to foreign capital and technology. Without that, the most likely path remains gradual decline rather than revival.

For global markets, Vakulenko says the implications are significant but not immediate. Even if Russian production were halved over two decades, the country would still rank among the world’s largest producers and exporters. Over time, however, shrinking oil income would weaken the foundations of Russian power.

“Russia currently has no other potential revenue source capable of replacing declining oil income,” he writes. The effect will be slow, he says, and “barely perceptible before the end of the current decade”, but in the longer run it would leave Russia poorer, less influential and more constrained in funding both military ambition and domestic stability.

Follow us online