Which countries in Europe and Asia have the most reserve coal-fired generating capacity in reserve?

Natural gas prices have already doubled since the start of the war in the Middle East and are expected to rise higher as the last of Qatar’s LNG exports arrive at their destinations.

That has left countries around the world to scramble for alternative sources of energy. As bne IntelliNews reported, coal is back as the easiest and fastest way to generate more power.

Which countries in Europe and Asia have the most reserve coal-fired generating capacity in reserve?

European buffers

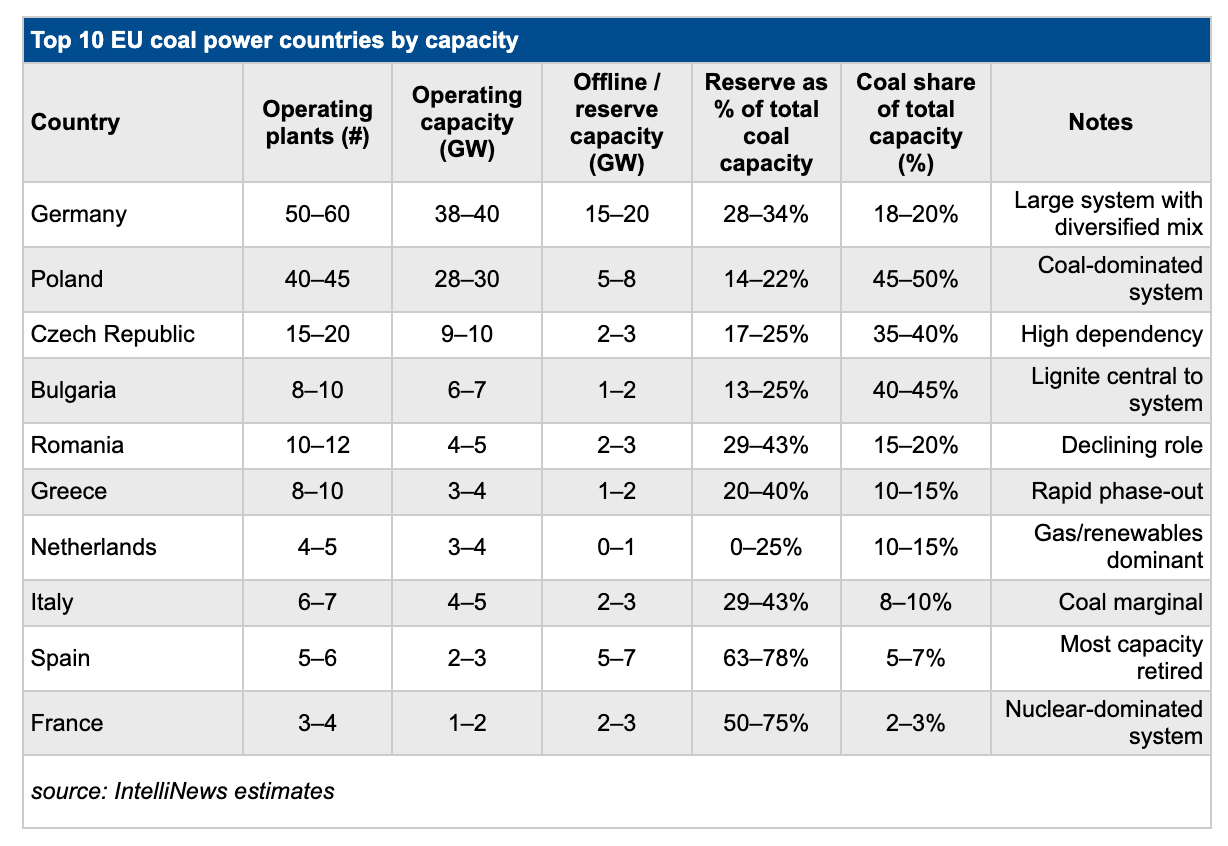

In Europe some of the biggest economies still make heavy use of coal but also have large reserves of offline coal-fired generating capacity thanks to the green energy transition.

Germany produces the most power using coal: 40GW with another 20GW, or 30% of the total generating capacity, in reserve giving it a big buffer to cope with gas price spikes.

The former socialist countries of Poland, Czechia and Bulgaria depend more heavily on coal, which accounts for between 35-50% of their total generating capacity. Thanks to energy transformation they have been winding down their dependence as they move steadily over towards renewables, giving all of them a buffer of between 20%-25% of coal-fired generating capacity that can be restarted in an emergency.

Romania, Greece and Italy are in even stronger positions with up to 40% of their total capacity offline, but Spain has emerged as the green transition champion with a massive 78% of its coal-fired capacity off line thanks to its rapid adoption of renewables. France has a similarly large buffer thanks to its switch to nuclear power which now accounts for 80% of its power generation.

As previously reported, the Nordic countries also have a significant buffer as they have already largely made the switch to green power. Currently, half of Europe’s power is generated from renewables and in Denmark 92% of power is now from renewables.

The coal buffer and the rapid rise of renewables leaves Europe much less exposed to the coming gas price spike than during the 2022 energy crisis.

The UK remains one of the most exposed as it closed its last coal-fired power station in 2024. As of last year, gas was the second most important source of energy, accounting for around 25-30% of the UK's electric generation and nuclear power providing another 11 to 14%, although renewables is expanding rapidly.

Asian buffers

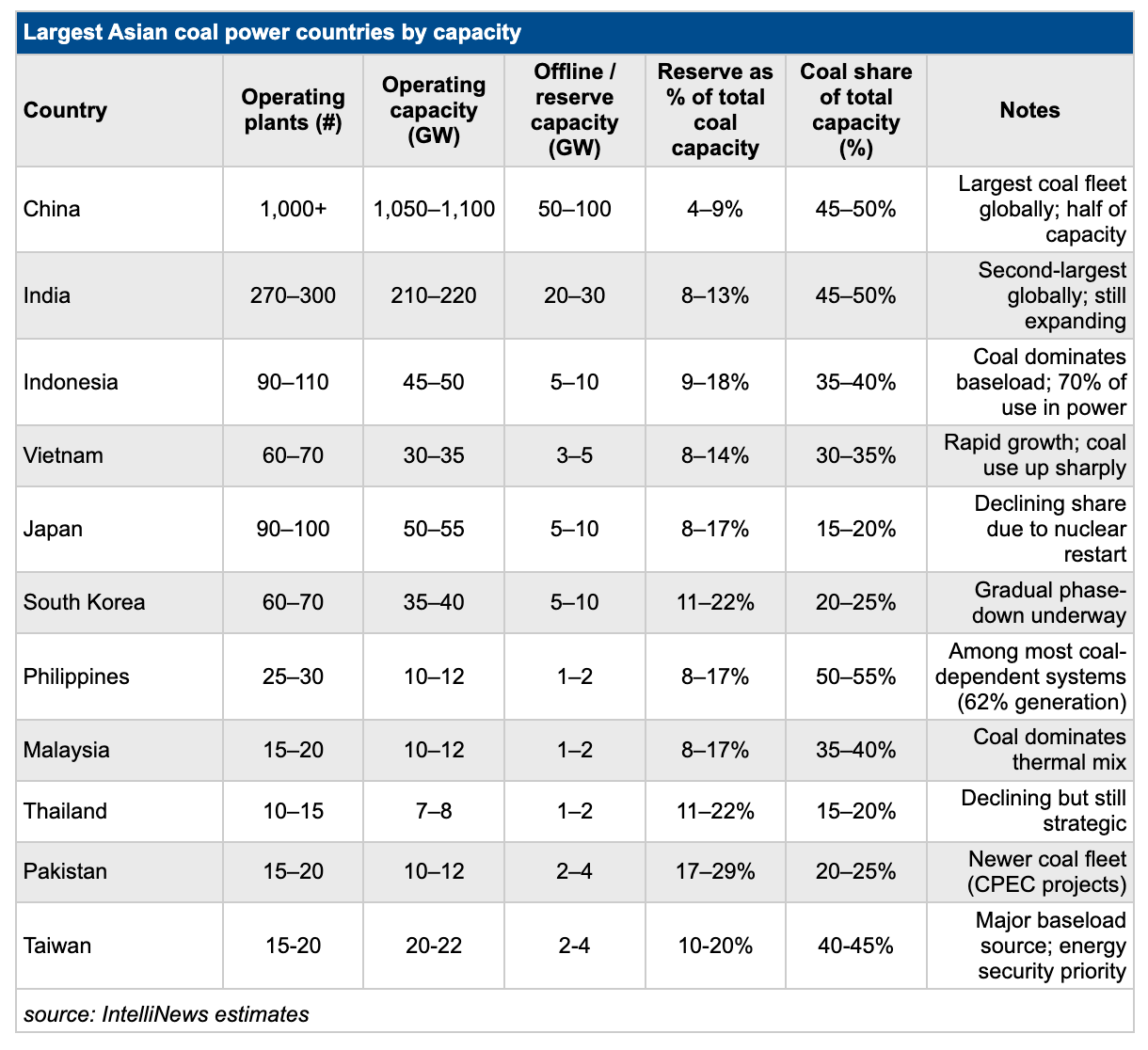

The story is similar in Asia, which remains much more dependent on coal than Europe, despite the fact that almost all the countries there have accelerated their adoption of renewables. China has emerged as the global green energy champion, but still generates half its power from coal and only as a 9% reserve of offline coal-fired power capacity.

China has been trying to wean itself off coal, but with economic growth running at over 6% for a decade, the process is going slowly. India still relies on coal for 75% of its energy needs, although it has also rapidly accelerated its roll out of renewables. It is also growing very quickly and that also means it has been unable to mothball much of its coal-fired capacity so only has a reserve of some 10% of offline coal stations. However, this week, Prime Minister Narendra Modi said the government has been laying in stocks of coal in preparation in case the unfolding gas crisis is protracted.

The situation is similar in the rest of SE Asia where coal plays a more important role than in Europe and offline capacity is around 10% of the total. In countries with a higher share, such as Thailand with some 20% of its coal-fired power capacity offline, the larger shares are usually due to the fact these countries were still in the process of switching to gas and not renewables.

Gas prices expected to surge

European gas prices are expected to remain elevated through 2026 following supply disruptions linked to conflict in the Gulf, Oxford Economics said in a note on March 24.

Storage shortages due to the big freeze this winter and constrained LNG flows as the last of Qatar’s seaborne deliveries reach their destinations in the next week will drive a prolonged shock, Oxford Economics says.

The consultancy said it had raised its forecast for the Dutch TTF benchmark to $58/MWh ($16.94/MMBtu) for the second quarter of 2026, a 61% increase from its pre-conflict baseline. Prices are projected to ease to $46/MWh ($13.5/MMBtu) by the fourth quarter, still 31% above earlier expectations, as “European buyers refill storage over the second quarter and the third quarter”.

European gas storage levels stood at 29% full, the lowest for this time of year since the 2022 energy crisis, adding to upward pressure on prices. Oxford Economics said “we expect this persistence of the price shock” as the EU attempts to rebuild inventories ahead of winter.

According to IntelliNews Lambda calculations, if restocking follows historical norms, Europe’s tanks will only be 75% full by the November 1 deadline, missing the mandatory 90% full under EU rules.

Despite the increase, analysts noted that markets are better positioned than during Russia’s invasion of Ukraine. “Our forecasts, and current future pricing, do not reflect a price shock of the magnitude that occurred when Russia invaded Ukraine in 2022,” the report said, citing expanded LNG supply, particularly from the US, and weaker industrial demand in Europe and China due to economic slowdowns in both places.

Global markets have nevertheless tightened sharply following disruptions to Gulf exports. Around 120bn cubic metres of gas — largely from Qatar — have been unable to transit through the Strait of Hormuz, exceeding the roughly 80bcm of Russian supply lost in 2022. Asian LNG benchmark JKM futures have risen by 90% since the start of the conflict. That led to a ten-fold increase in TTF gas prices to €300MTh.

Qatar’s Ras Laffan liquefaction facility has been shut since March 2 and could take four to six weeks to restart if a ceasefire deal is agreed. US President Donald Trump said on March 23 that the White House was in talks with Tehran on a possible 15-point plan to end hostilities.

Oxford Economics believe Asian buyers are expected to face the greatest impact. “Asian buyers are disproportionately affected by the loss of Gulf gas exports and will face higher prices as they compete to divert US LNG cargoes from Europe to Asia,” Oxford Economics said.

Countries heavily reliant on LNG imports, including Taiwan and Pakistan, may be forced to curb consumption or switch to more carbon-intensive fuels, as limited supply pushes up both gas and power prices.

Follow us online