Falling electrotech costs create a fast catch up path for Global South

A new energy pathway is emerging for developing economies, one that challenges the assumption that fossil fuels are a prerequisite for growth, according to a new report by Ember.

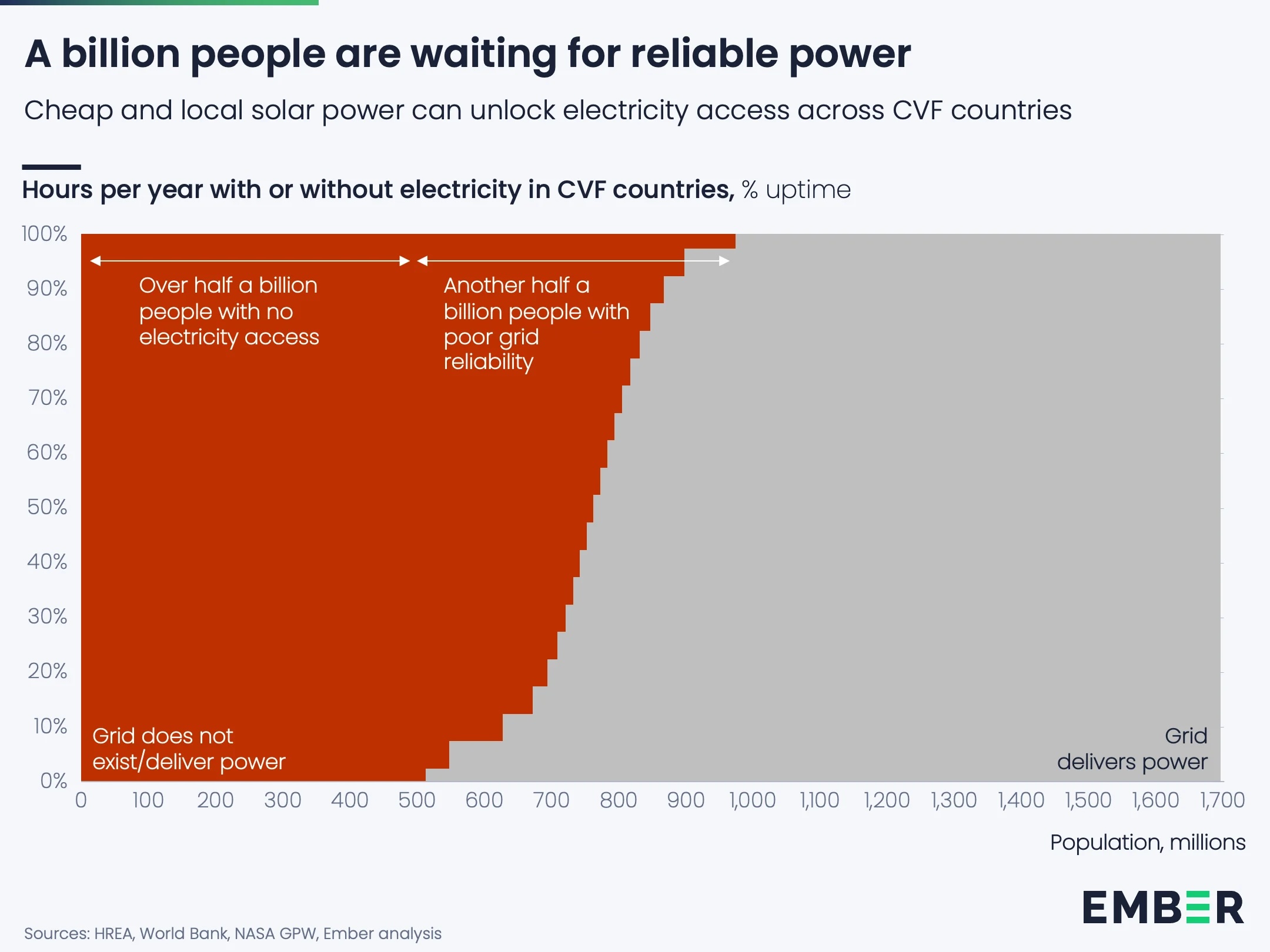

More than 700mn people still lack access to electricity, while many more face unreliable supply, despite decades of fossil-fuel-led development. But tumbling costs and increased availability of solar panels and long lasting batteries are changing the face of the utilities sector making cheap electricity available to billions of the world’s poorest people.

With global energy still heavily reliant on fossil fuels, the cost of importing gas and oil accounts for approximately 3% of GDP in poor countries, according to another Ember study, a heavy budgetary weight on developing countries. And these supplies usually come with geopolitical dependencies as the war in Iran has shown. However, once the initial capital has been sunk in renewables, they are essentially a free source of power and have no supply dependencies at all as the sun shines everywhere.

The gap between power supply and demand is particularly stark across the 74 nations of the Climate Vulnerable Forum (CVF), which together account for over a fifth of the global population but less than 5% of electricity demand and GDP. These countries represent roughly three-quarters of people living on less than one MWh of electricity per capita. “The conventional fossil-based development model has failed to reach them at scale,” Ember said, citing high capital costs and weak state capacity as structural barriers.

A reversal in the economics of energy

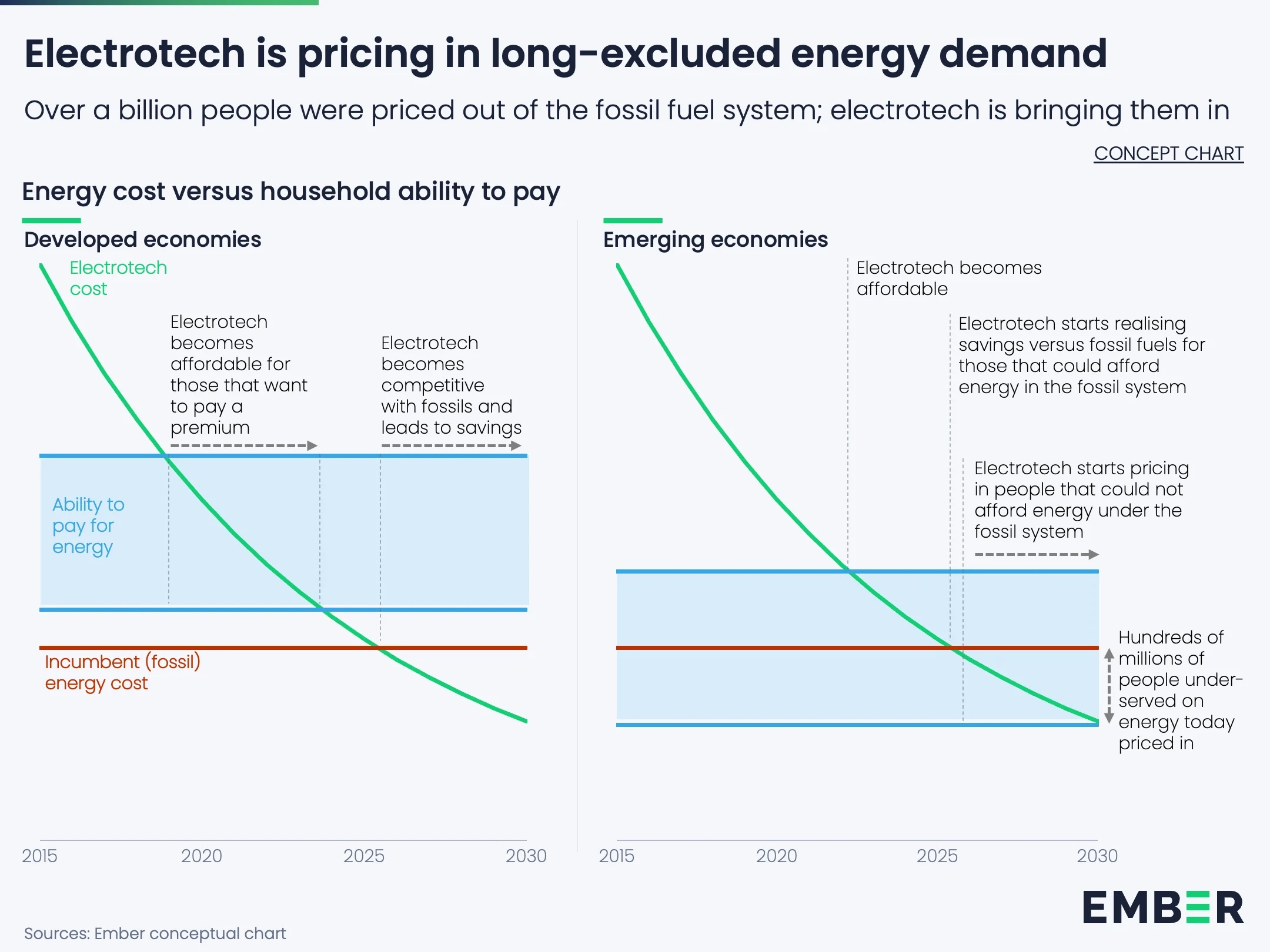

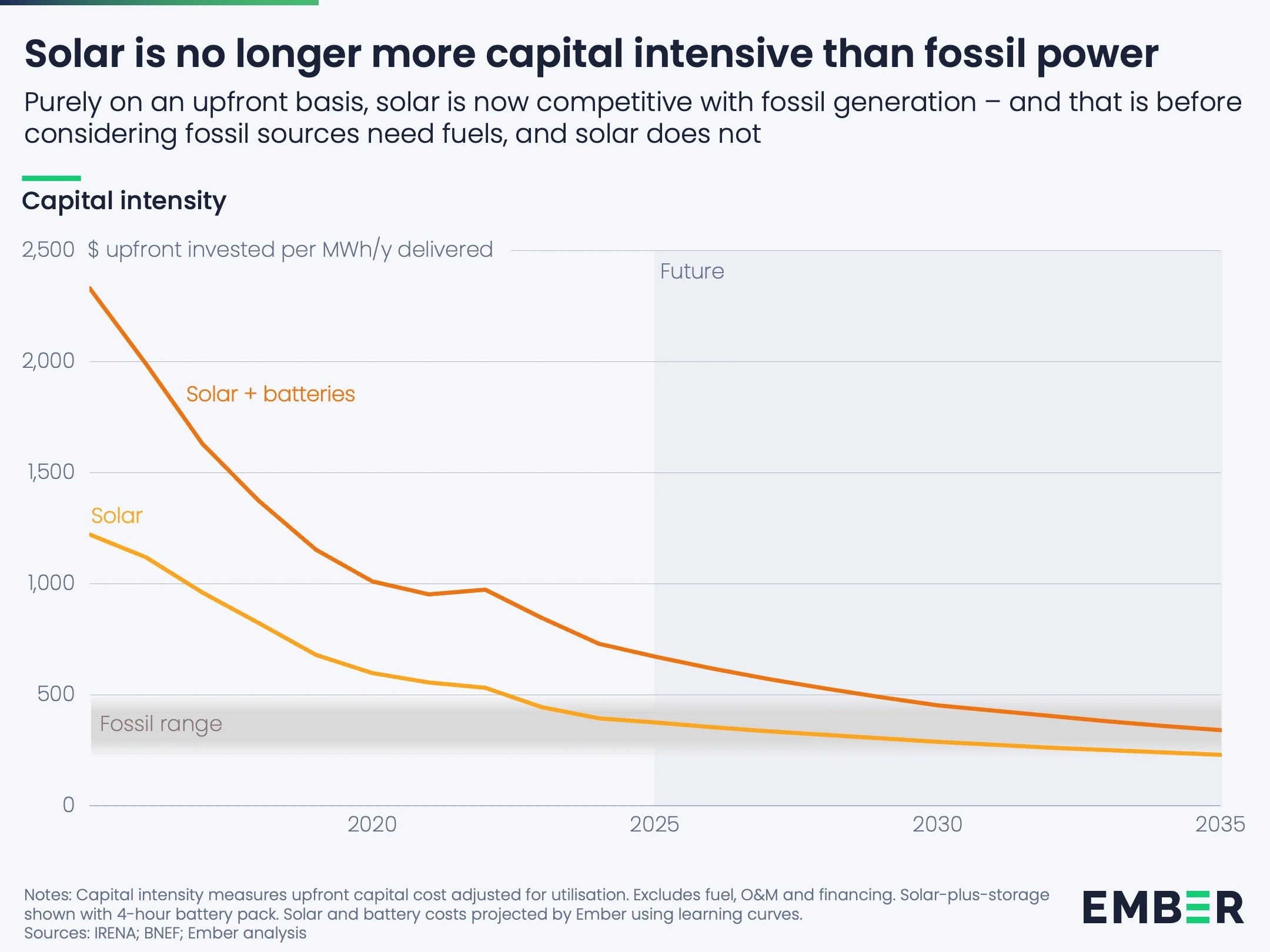

At the centre of the shift is a rapid change in cost dynamics. “A decade ago, a solar plant could require up to five times the upfront investment of a comparable coal or gas plant,” Ember notes. That relationship has now inverted: solar is competitive on capital expenditure alone, with solar-plus-storage, thanks to the parallel battery revolution, expected to follow by 2030 and undercut fossil alternatives by 2035. The revolution has been that renewables is now the cheapest source of energy on the planet.

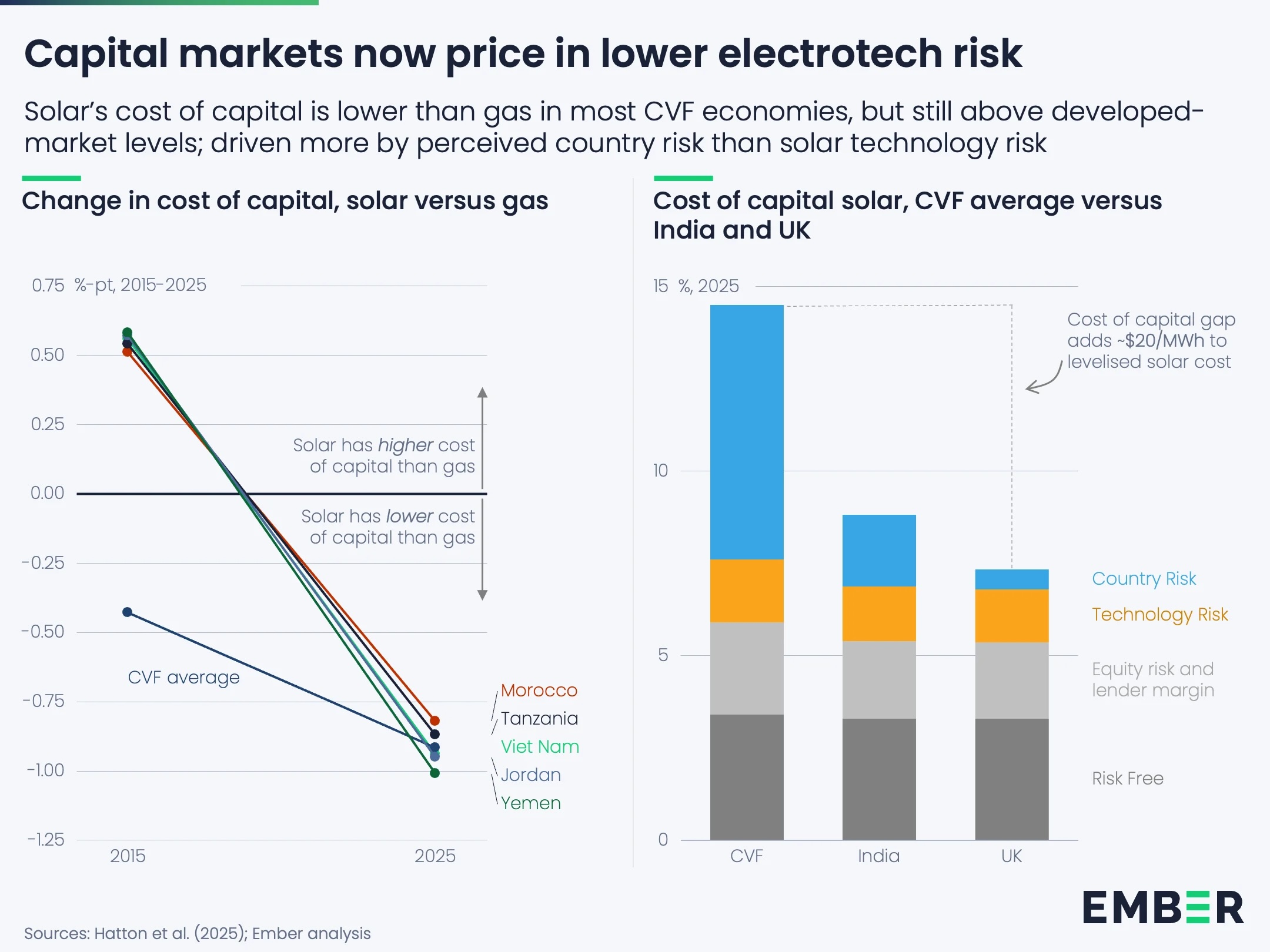

Financing trends have reinforced this shift. In Morocco, the cost of capital for solar held at 8.7% between 2015 and 2025, while gas rose from 8.2% to 9.6%. In Vietnam, solar financing fell from 12% to 10%, below gas at around 11%. While borrowing costs in CVF countries remain roughly double those in advanced economies, Ember notes that reflects country risk rather than technology.

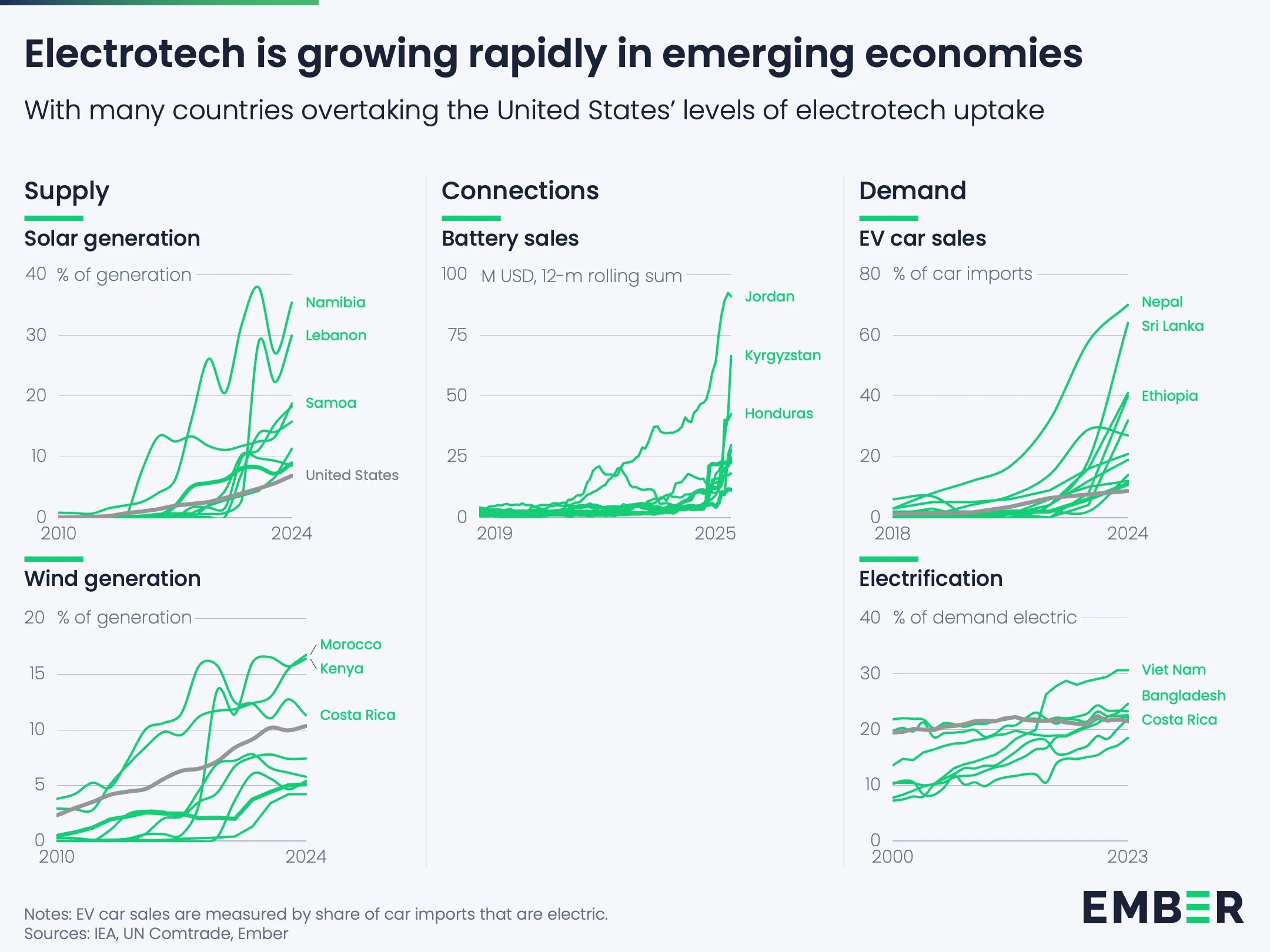

Leapfrogging across supply and demand

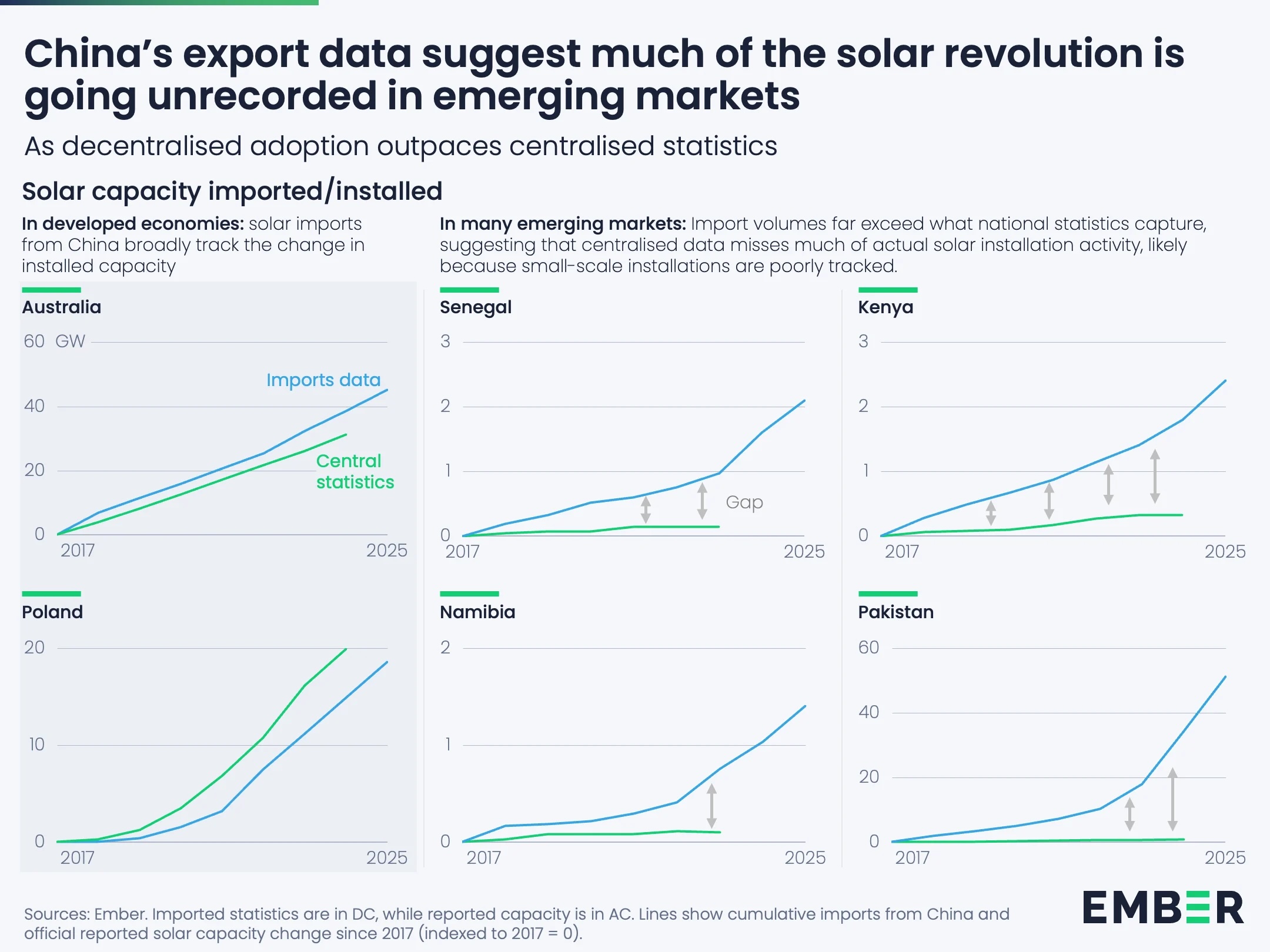

Adoption is already outpacing expectations. “46% of CVF nations, measured by electricity demand, have overtaken the United States in solar penetration,” Ember states, while about 51% have surpassed it in electrification. In eight out of ten CVF countries, cumulative solar imports since 2017 are at least three times higher than officially recorded installed capacity.

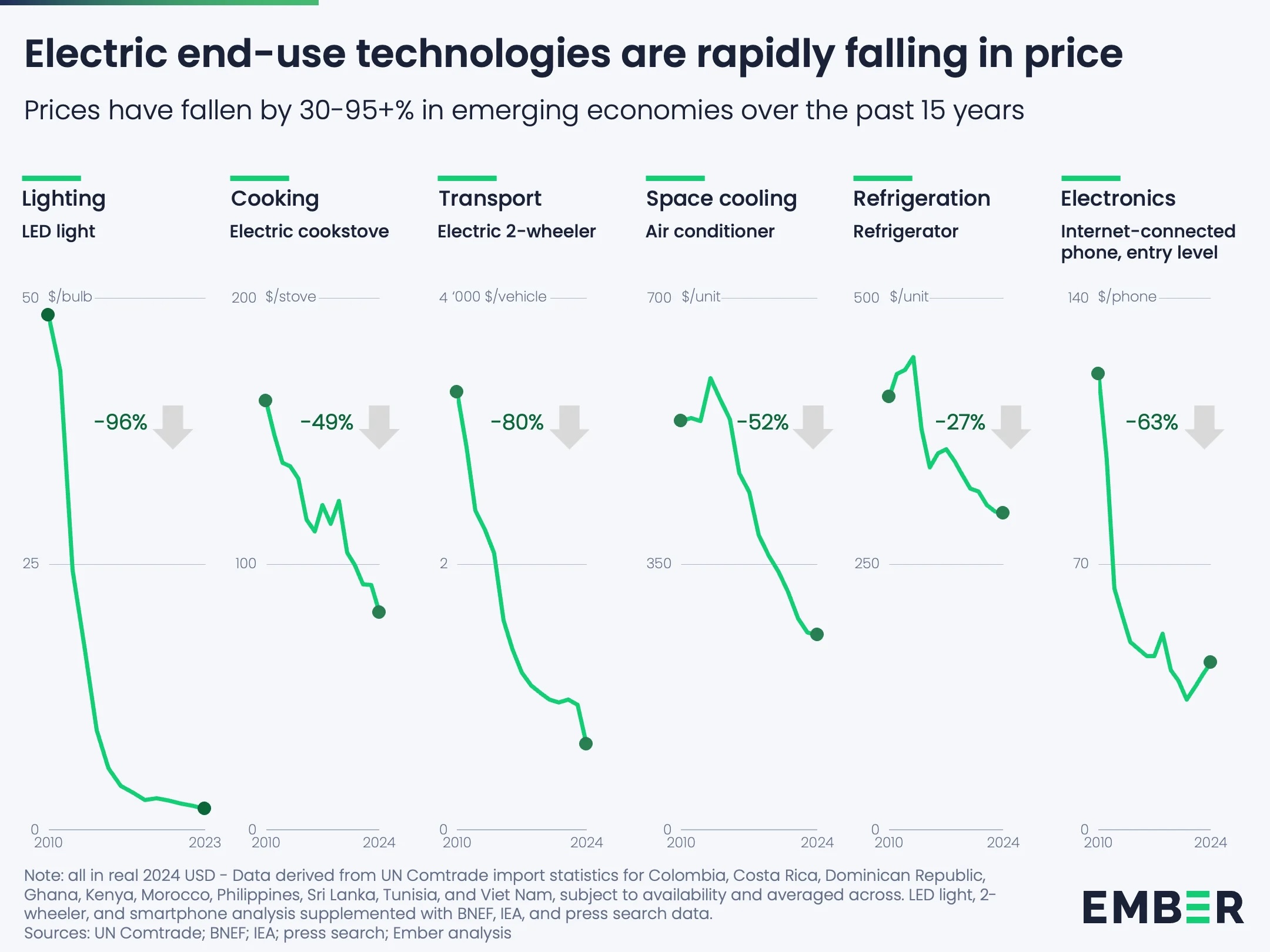

Costs are falling sharply across end-use technologies. Prices for electric solutions — from two-wheelers to cooling systems — have declined by between 30% and 95% over the past decade. “The interesting shift is not petrol to electric; it is no bike to e-bike,” Ember observes, highlighting the expansion of first-time energy access rather than simple substitution as emerging economies go straight to the state-of-the-art solutions to traditional problems.

Decentralisation and the ‘last mile’

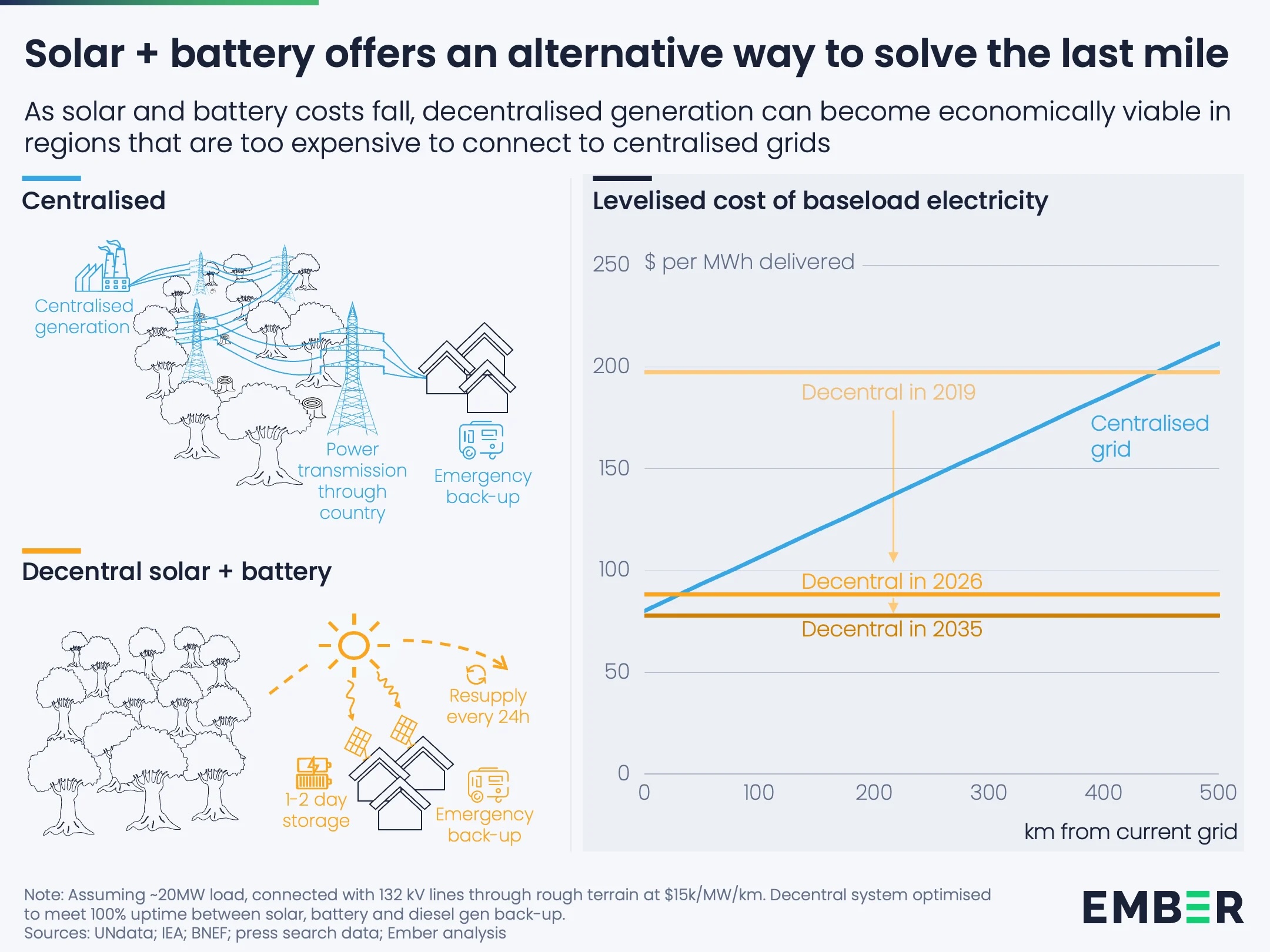

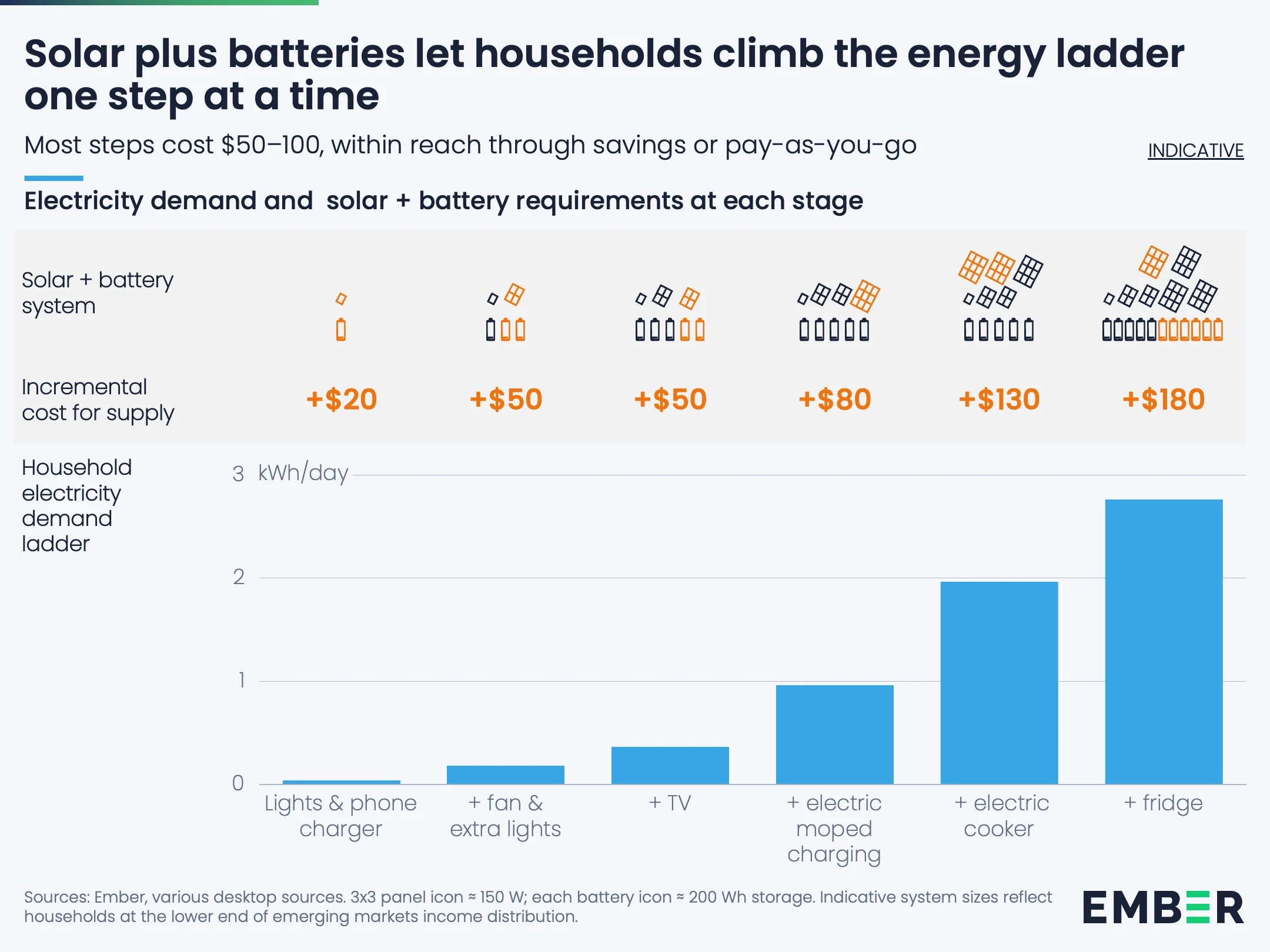

Falling battery costs are transforming electricity access. The drawback that has held the rollout of renewables back is the “baseload” problem. The production of wind and solar power is uneven and unreliable so that countries need to keep traditional fossil fuel power stations in reserve to meet demand when the sun is not shining or the wind is not blowing. The rapid expansion of grid level battery storage is eating into this problem, allowing grid operators to store power for later. That is still a work in process and will not be complete until the grid-level eight-hour battery appears to complete the green revolution.

In 2019, solar-plus-storage systems were only viable more than 400km from the grid. By 2026, “solar-plus-storage is already cheaper than grid extension for any community more than a few tens of kilometres from existing lines,” Ember states.

The decentralised model mirrors the spread of mobile phones over fixed-line networks. Small-scale systems can be deployed incrementally, reducing the need for large upfront investment. However, Ember cautions that maintenance ecosystems remain underdeveloped, with product failures in some markets highlighting the need for local service capacity.

From import dependence to electric abundance

The macroeconomic implications are significant. China is the textbook example and is emerging as the world leading electrostate. It has invested heavily in renewables and is on track to produce an abundance of low-cost power to fuel its ongoing rapid growth.

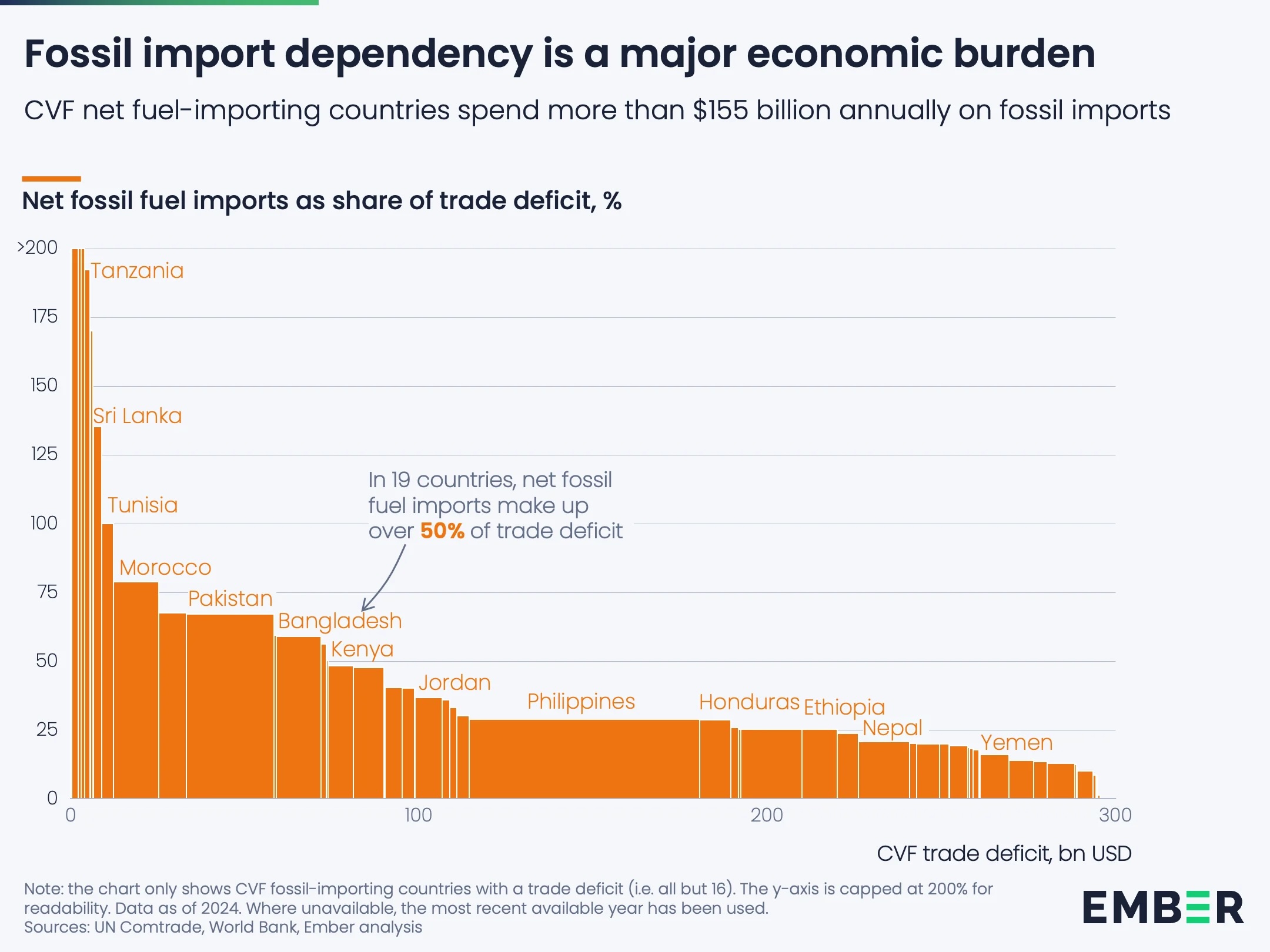

The switch to renewables will drastically alter the balance of payment accounts in any country making the change. Net fossil fuel importers within the CVF spent $155bn on imports in 2024, with fossil fuels accounting for more than 50% of trade deficits in 19 countries. Morocco’s figure stands at 79%, Pakistan’s at 67% and Bangladesh’s at 59%.

By contrast, solar potential is vast. Ember estimates that CVF countries could generate more than 320 MWh per capita annually from solar resources — over 25 times current per capita consumption in the United States. Existing deployments are already reducing import dependence: 138 GW of solar panels imported between 2020 and 2025 could displace up to $20bn in LNG or $42bn in diesel imports each year.

The transition also carries geopolitical implications. “Solar and wind power provide energy that does not need to be imported, priced abroad, or paid for in foreign currency,” Ember states. CVF countries hold three assets critical to the transition — minerals, manufacturing potential and growing consumer markets — attracting competing interest from China, the United States and Europe. The rise of renewables will also undermine the petrodollar system where countries need to hold a reserve of dollars to pay for oil imports in deals that are exclusively denominated in dollars. Shedding the need to import dollars means more countries can settle trade deals in mutual national currencies, provided they run a relatively balanced trade account with their main partners – another trend that has emerged in the last few years.

Yet Ember cautions that resource endowments do not automatically translate into value capture, pointing to the Democratic Republic of Congo’s limited gains from cobalt extraction as a warning.

A narrowing window of choice

For many emerging economies, the decision point is immediate. Most CVF countries remain dominated by biomass rather than fossil infrastructure, limiting lock-in. “Falling electrotech costs now make the direct path from biomass to electricity affordable,” Ember states.

“The choice is now between the electrotech fast-track and the fossil detour,” it adds, arguing that the opportunity to bypass decades of fossil dependency remains open, but may not persist indefinitely.

Follow us online