Fitch raises 2026-2027 oil and gas price assumptions on prolonged Hormuz closure

_2.jpg)

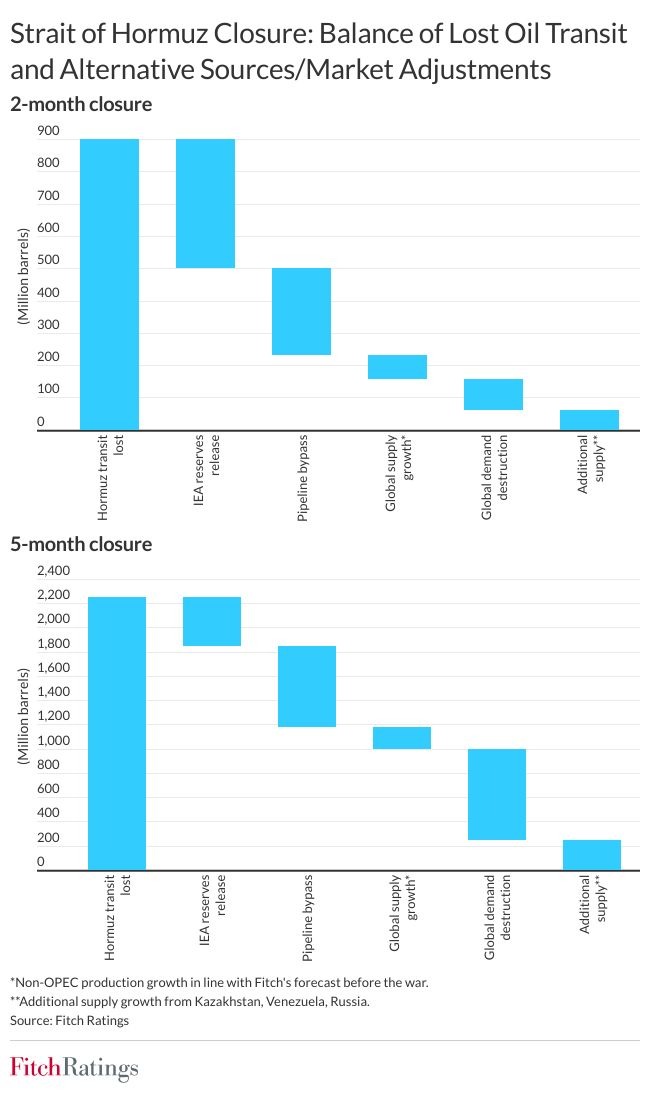

Fitch Ratings has raised its 2026 and 2027 oil price assumptions on the basis of a longer-than-expected effective closure of the Strait of Hormuz, with the agency now assuming the waterway will begin reopening around July, Fitch Ratings said on May 11.

The agency expects Brent crude to remain at USD100-110 per barrel between May and July during the closure, before falling to USD70 per barrel by September, a level driven by supply and demand with a residual premium.

Before the war, 15mn barrels per day (bpd) of crude oil and 5mn barrels of oil equivalent per day of refined products transited the strait, accounting for around 20% of global oil consumption, Fitch Ratings said.

The agency had previously assumed the effective closure would last one to two months, but has now extended that period to about five months as the key driver of its revised oil price assumptions. Average annual oil prices are likely to be lower if the closure ends sooner, the agency said.

Fitch Ratings expects a quick recovery in production following the reopening, with no material damage reported to oil infrastructure. Oil stored on tankers is likely to be sold first, followed by the return of curtailed production, with output expected to ramp up to broadly normal levels within several weeks.

The Organisation of the Petroleum Exporting Countries (OPEC) is likely to produce up to maximum capacity to offset volumes lost during the closure, the agency said. OPEC spare capacity stood at 3.6mn bpd before the conflict.

Non-OPEC supply is expected to grow by around 3mn bpd, including 1.2mn bpd from the United States and Latin America that Fitch Ratings had forecast previously, plus a further 1mn bpd from Kazakhstan and Venezuela. Higher prices would also incentivise production growth in the US and Russia.

The market adjusted in March and April through the release of 400mn barrels of oil reserves by the International Energy Agency (IEA) and demand destruction of 1.6mn bpd, equivalent to 1.5% of global demand, alongside non-OPEC production growth and the use of bypass pipelines in Saudi Arabia and the United Arab Emirates. The spare capacity of those two pipelines stood at 4.5mn bpd before the conflict, the agency estimated.

Under the agency's current assumption of a five-month effective closure and no further inventory drawdowns, demand destruction of 5mn bpd, or 5% of global demand, would be required to balance the market during the closure period. Additional inventory releases would likely reduce that figure.

Fitch Ratings described that level of demand destruction as severe but achievable, citing the growing share of consumption from the oversupplied petrochemicals sector and disruption to jet fuel demand from flight cancellations and high prices. Most petrochemicals capacity growth is in Asia, which is also the key consumer of oil transiting Hormuz.

Global oil stocks stood at 8.2bn barrels in January, a very high level comparable to that seen in 2020 and sufficient to offset disrupted Hormuz volumes for more than a year. China held 1.2bn barrels, which could cover its Hormuz-linked imports for over eight months until the end of October, the agency said.

The agency raised its 2026 and 2027 Title Transfer Facility (TTF) gas price assumptions on disrupted liquefied natural gas (LNG) flows from Qatar through the strait and damage to the country's LNG infrastructure. Assuming the strait reopens around July, the European gas market will remain tight throughout 2026.

Henry Hub assumptions were left unchanged, reflecting limited spare US liquefaction capacity and constraining US producers' ability to benefit from higher gas prices elsewhere.

Follow us online