Gulf oil output could recover within months of Hormuz reopening, Goldman Sachs says

Gulf crude oil production could recover to close to pre-war levels within a few months of the Strait of Hormuz safely reopening, according to Goldman Sachs (NYSE: GS).

The bank assessed the physical constraints on production recovery and the significant risks, concluding that a full return to pre-war output levels may prove elusive, particularly if the closure persists.

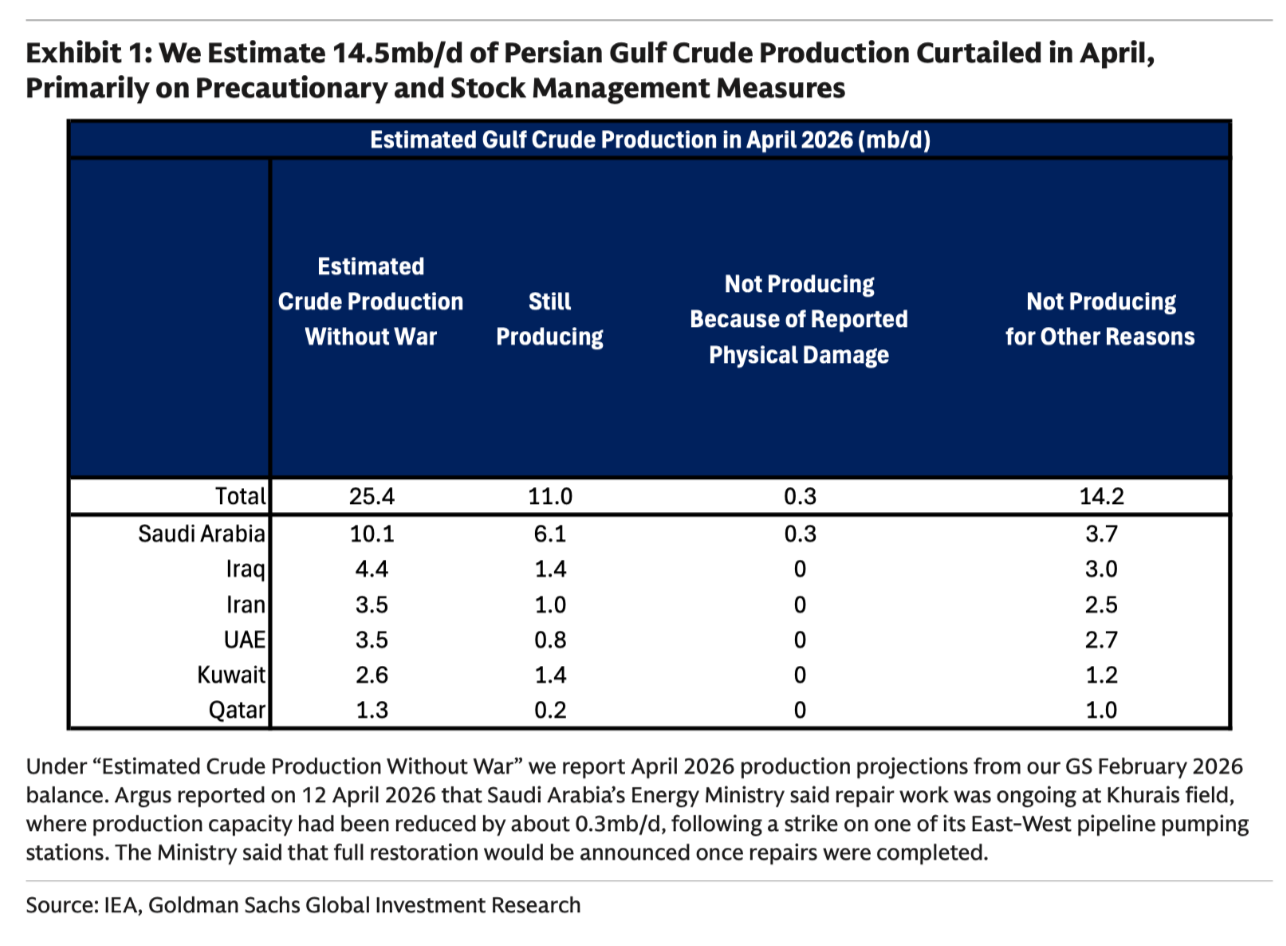

Goldman estimates that approximately 14.5mn barrels per day of Persian Gulf crude production — equivalent to 57% of pre-war output — is currently curtailed, with the vast majority of that reduction driven by precautionary measures and stock management rather than physical damage to oil infrastructure. The distinction matters enormously for the recovery outlook: fields that have been shut in as a precaution can in principle be reopened relatively quickly, while those that have sustained physical damage face a more complex and uncertain path back to production.

Saudi Arabia accounts for the largest share of curtailed output. Of its estimated pre-war production of 10.1mn barrels per day, Goldman calculates that 6.1mb/d is still flowing, exported via is westward pipelines, while 3.7mb/d has been shut in for reasons other than reported physical damage and 0.3mb/d has been lost to confirmed infrastructure damage. Specifically, a strike on one of the East-West pipeline pumping stations at the Khurais field, which Saudi Arabia's Energy Ministry said in April had reduced capacity by 0.3mb/d, with full restoration to be announced once repairs were complete. Iraq, Iran, the UAE, Kuwait and Qatar account for the remainder of the curtailed output.

The case for a solid recovery

Goldman identifies three grounds for cautious optimism about the pace of recovery once the Strait reopens. First, the evidence of physical damage to oil fields remains limited relative to the devastation visited on LNG infrastructure, where QatarEnergy's Ras Laffan facilities sustained significant damage. The oil fields appear, for the most part, to have been shut in rather than destroyed.

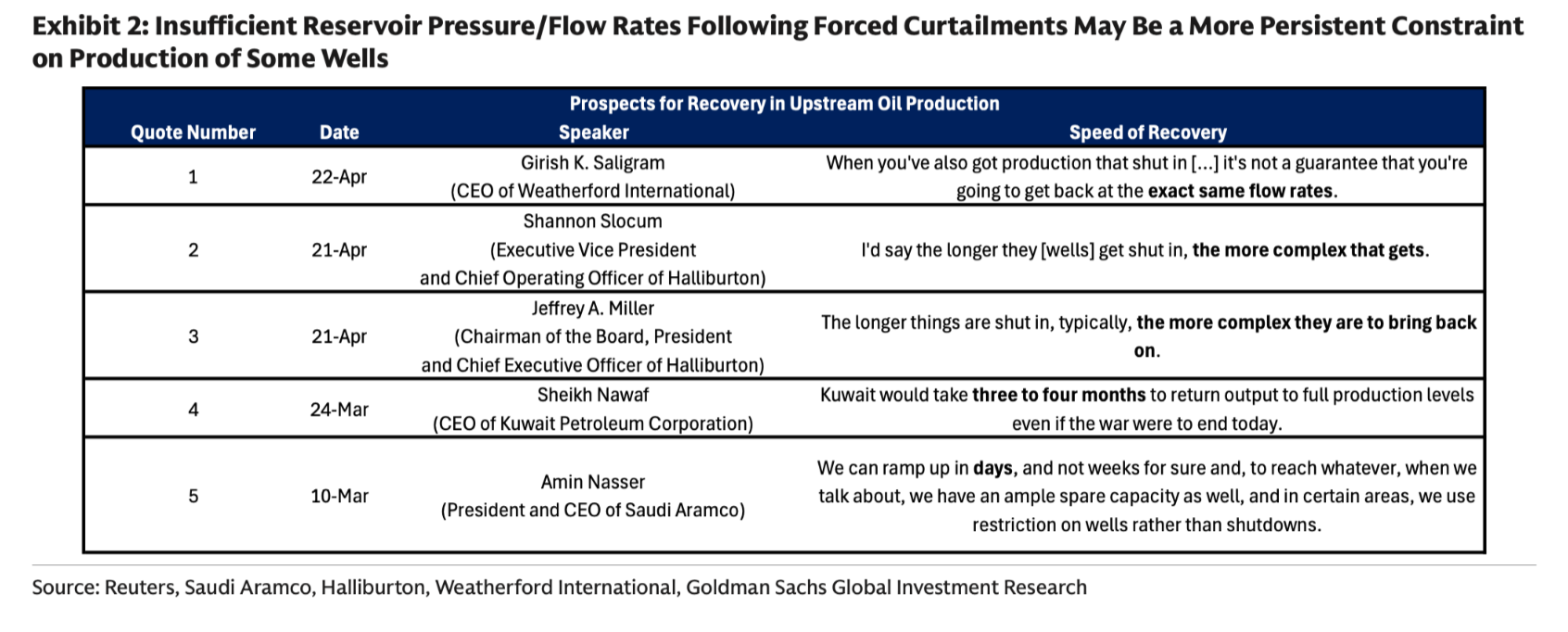

Second, the bank points to comments made by Amin Nasser, president and chief executive of Saudi Aramco (TADAWUL: 2222), in March. "We can ramp up in days, and not weeks for sure," Nasser said, adding that Saudi Arabia had "ample spare capacity" and that in certain areas the company had used "restriction on wells rather than shutdowns" — a mode of curtailment that is considerably easier to reverse than a full well closure.

Third, historical precedent supports the view that Saudi Arabia and the UAE tend to deploy available spare capacity to stabilise markets following major supply disruptions. Goldman's analysis of five historical episodes — including the Gulf War of 1990-91, the Libyan civil war, the first wave of Iran nuclear sanctions and the Abqaiq drone attack of 2019 — shows that core OPEC producers have consistently moved to offset disrupted supply from other sources, though the pace and extent of recovery has varied considerably across episodes.

Goldman estimates that Saudi Arabia and the UAE together could deploy over 2mb/d of spare production capacity above pre-war levels to stabilise markets after a safe and full reopening of the Strait. An average across external forecasts from Rystad Energy, the IEA and the EIA projects recoveries of 70% of lost production within three months of reopening, and 88% within six months.

The constraints that could slow recovery

The more sobering part of Goldman's analysis concerns the bottlenecks that could prevent a smooth or rapid production ramp even after the Strait reopens. The bank identifies two primary physical constraints: transportation capacity and well flow rates.

On transportation, Goldman estimates that available empty tanker capacity in the Persian Gulf has fallen by approximately 50% — equivalent to around 130mn barrels of capacity — since the start of the war, as vessels loaded with oil already produced have accumulated in the Gulf with nowhere safe to go. When the Strait reopens, those laden vessels will need to destock before empty tankers can be used for new production, temporarily constraining the pace at which new output can reach market. The historical peak for oil flows through Hormuz was 23.3mb/d, recorded in June 2018, against a normal throughput of around 20mb/d — suggesting the infrastructure can handle a surge, but only once the backlog clears.

On well flow rates, Goldman draws on a series of candid assessments from oilfield services executives. "When you've also got production that shut in, it's not a guarantee that you're going to get back at the exact same flow rates," said Girish Saligram, chief executive of Weatherford International (NASDAQ: WFRD). Shannon Slocum, executive vice president and chief operating officer of Halliburton (NYSE: HAL), was more direct: "I'd say the longer they get shut in, the more complex that gets." Her chairman and chief executive Jeffrey Miller agreed: "The longer things are shut in, typically, the more complex they are to bring back on."

The mechanism is geological. Forced curtailments can lead to reservoir pressure falling below levels needed to sustain prior flow rates, requiring intervention and workover jobs — essentially well maintenance operations — before production can be restored. The severity of this problem varies by reservoir type, but Goldman notes that Iran and Iraq have a higher share of production from relatively low-pressure reservoirs than other Gulf producers, making their fields more vulnerable to prolonged shut-in. Kuwait has already acknowledged the challenge: Sheikh Nawaf, chief executive of Kuwait Petroleum Corporation, said his country would take "three to four months to return output to full production levels even if the war were to end today."

The long-closure risk

Goldman is explicit that its relatively optimistic base case depends critically on the assumption that the Strait reopens in coming months and that there are no renewed strikes on oil infrastructure. The longer the closure continues, the more pessimistic the recovery trajectory becomes — reflecting more workover requirements, slower procurement of depleted inputs such as drill pipes, and the tanker destocking constraint persisting for longer.

In a prolonged closure scenario, Goldman sees significant risks that the recovery is only partial. Large differences across Gulf fields in reservoir characteristics, infrastructure sophistication and maintenance standards mean that the aggregate recovery trajectory will be uneven — with Iran and Iraq facing the most complex paths back to full production, and Saudi Arabia and the UAE the most straightforward.

The bank also flags the risk of "scarring", permanent damage to production capacity of the kind documented in several of the five largest historical oil supply shocks, as a tail risk that grows the longer hostilities continue and the more complex the well-intervention requirements become.

For now, markets are trading on the assumption that a ceasefire and Hormuz reopening remain achievable within months. Goldman's analysis suggests that assumption is broadly consistent with a solid, if incomplete, production recovery, provided the closure does not stretch beyond the summer.

Follow us online