ING: Asia’s outlook under higher oil prices

Heavy dependence on Middle Eastern oil leaves Asia vulnerable to sustained supply shocks. While inflation risks remain largely manageable at the moment given a low starting point, higher import bills will result in weaker trade balances with some currencies like PHP, THB, INR and KRW more vulnerable.

For now, Asia seems able to absorb the recent jump in oil prices. Inflation across much of the region is starting from relatively low levels and has generally been well contained. But the real question is how high and how long prices stay elevated – because that’s what will ultimately determine the economic fallout.

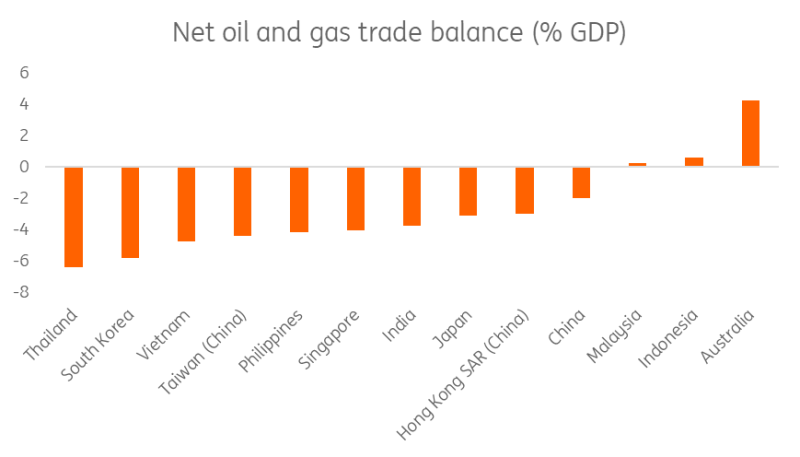

Asia is especially vulnerable to sustained oil price shocks. The region relies heavily on imported energy: apart from Malaysia and Australia, every major economy runs a sustained deficit in oil and gas trade, leaving them exposed when global prices surge. If higher prices persist, three factors will shape the impact.

Heavy dependence on Middle Eastern oil

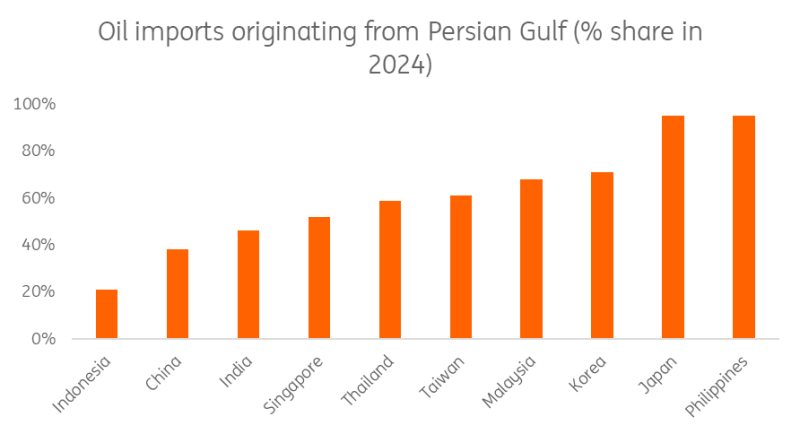

A significant share of Asia’s crude supply comes from the Persian Gulf. Japan and the Philippines rely on the region for almost 90% of their oil needs, while China and India import roughly 38% and 46% respectively. Any disruption in the Strait of Hormuz – a critical shipping lane – would restrict supply, potentially causing shortages that slow business activity and put pressure on manufacturing across Asia.

Over 90% of Japan and Philippines' oil imports come from the Middle East

Source: United Nations, WTO

A double-edged sword for trade

Even without a physical supply disruption, higher global oil prices worsen trade balances and add to inflation pressures. Thailand, Korea, Vietnam, Taiwan, and the Philippines are the most exposed. A mere 10% rise in oil prices can deteriorate current account balances by 40–60 basis points. Prolonged increases would only deepen these deficits. The key beneficiary should be Australia, the only large exporter of oil and gas in the region.

It’s not just the higher oil import bill that hurts – some Asian economies could also see their export growth take a hit. In recent years, many Asian exporters have been actively diversifying away from the US market because of rising US tariffs, and the Middle East has emerged as an important alternative growth destination. That makes the region’s recent instability especially concerning. India is the most exposed to the Middle East-driven export demand, with China following closely behind. Any prolonged disruption in the region risks slowing this new export channel just as it was starting to gain momentum.

GCC export disruptions add another risk to Asia’s trade balances

Source: CEIC

Weaker trade balances will put renewed pressure on Asian currencies

Even a short-lived jump in oil prices can have an outsized impact on FX markets. Recall how the less than two-week oil price spike in June 2025 was enough to pull down the PHP, KRW, THB, and JPY by roughly 1.5–3%, despite the brief nature of the conflict. While inflation didn’t move much then because the conflict was so brief, a more prolonged period of elevated oil prices would be a very different story. A prolonged conflict, coupled with continued currency weakness, would feed more directly into inflation pressures across the region. And with Asia’s heavy reliance on imported energy, currencies like the Thai baht, Korean won, Philippine peso, and Indian rupee remain particularly vulnerable to swings in oil prices and sustained deterioration in trade balances.

Asia runs large energy trade deficits

Source: United Nations, WTO

Strong inflation pass-through is possible – but fiscal cushions can help

Because energy makes up a relatively large share of consumer inflation baskets across emerging Asia, higher oil prices can, in theory, push headline inflation up quickly, especially as higher fuel costs often drive food prices higher too. Emerging Asia has 25-45% of its CPI baskets driven by food. That’s why the most exposed economies, like India and the Philippines, are particularly vulnerable, where a 10% jump in oil prices could raise inflation by as much as 0.4 percentage points.

That said, the impact is far from uniform across the region. Several economies like Indonesia, Thailand and India are still partially shielded by fuel subsidies or regulated pricing, which dampens the direct pass‑through from global oil markets. On the other hand, the Philippines – also the worst impacted by higher oil prices – tends to see a stronger inflation hit because retail fuel prices are more market-driven and subsidies are limited.

Our base case had inflation across Asia rising but still staying within most central bank targets. But a price shock of this magnitude – if it lasts – coupled with currency depreciation could push inflation, for example, in the Philippines to the upper end of Bangko Sentral ng Pilipinas's 2-4% inflation target, increasing the pressure on the central bank to hold rates instead of cutting further. Countries like Indonesia and India, which benefit from fuel subsidies, should still retain some room to ease, though the probability of further cuts would be lower.

Content Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Follow us online