Inventory drawdowns mask impact of Hormuz disruption as clock runs down towards a September supply crunch

Global oil markets are relying heavily on inventory drawdowns to offset a supply shock caused by the closure of the Strait of Hormuz, with OECD stockpiles potentially reaching stress levels by mid-September if current trends persist, according to Oxford Economics.

The consultancy estimates that around 14mn barrels per day (mbpd) of oil that would normally pass through the Strait of Hormuz was removed from the market in April from a total of 20mbpd pre-war, after accounting for available bypass pipeline capacity. Additional output from producers outside the Gulf and an existing market surplus reduced the effective supply loss to roughly 10mbpd, while higher prices cut demand by about 3mbpd. The remaining shortfall of approximately 5.7mbpd has been met through inventory drawdowns.

“This adjustment explains why shortages have not yet become acute,” Oxford Economics said. “The market has not had to replace the full loss of Hormuz flows, instead relying on demand destruction, additional non-Gulf supply, and inventory drawdowns to absorb the remaining gap.”

Global oil inventories are declining at a record rate as the market absorbs a major Middle East supply disruption but these mitigating factors mean there is still some wiggle room and oil prices, while elevated, have not reached the catastrophic levels predicted by some at the start of the conflict in February.

The Strait of Hormuz, located between Oman and Iran, handles roughly a fifth of global oil consumption under normal conditions. A prolonged disruption would place sustained pressure on both physical supply chains and global economic growth.

Oxford Economics argued that the key issue is not the complete exhaustion of inventories but the point at which stock levels become low enough to trigger defensive behaviour among governments, refiners and traders.

Global oil inventories stood at approximately 7,950mn barrels in April, while OECD industry and government stocks totalled 3,889mn barrels, including 2,712mn barrels held by industry.

Inventories become stressed when OECD industry stocks fall below 52 days of forward demand, equivalent to 2,308mn barrels. Based on current drawdown rates of 146mn barrels per month, OECD industry inventories would reach that threshold by mid-September, which would induce fresh panic and spiking prices.

However, that deadline might be extended to January 2027 depending on how big the effects of demand destruction are.

“The IEA reported that global oil demand fell by 3mbpd to 101.3mbpd in April. Given that prices had increased by 84%, this implies an elasticity of -0.03, in line with our earlier expectations. Crude supply from outside the Gulf increased by 1.6mbpd, implying a supply elasticity of 0.02,” Oxford Economics reports.

Over time, market participants could adjust further to higher prices, as these responses occur with a lag. Consumers can reduce fuel demand by changing behaviour or switching technologies, but decisions such as purchasing an EV take time to feed through. Producers also face lead times when drilling new wells or expanding supply, while refiners and other midstream participants need time to optimise operations, for example by prioritising transport fuels.

In addition, the rapid roll out of green energy sources is working to reduce the demand for oil and gas. Renewables have already saved Europe €100mn every day since the start of the Iran war as now half of Europe’s power is generated from renewable sources – and that capacity will continue to grow.

“This suggests that the demand and supply response could increase over time, which would reduce the pull on inventories. Indeed, a 50% increase in this adjustment would reduce the draw on inventories to 3.3mbpd (Chart 2), extending the run room to January 2028,” Oxford Economics said.

The International Energy Agency’s co-ordinated release of an all-time record 400mn barrels of oil from strategic reserves has already helped cushion the market. Oxford Economics noted that 310mn barrels remain available from the 400mn total, which should continue to support industry inventories until September.

The consultancy said emerging economies in Asia-Pacific and Africa face the greatest risk of shortages because they are less able to compete for increasingly expensive replacement supplies. By contrast, developed OECD economies are generally better positioned to secure available cargoes at prevailing prices.

Oxford Economics said pressure on Washington and Tehran to reach a ceasefire deal as the technical minimum OECD inventory levels are approached.

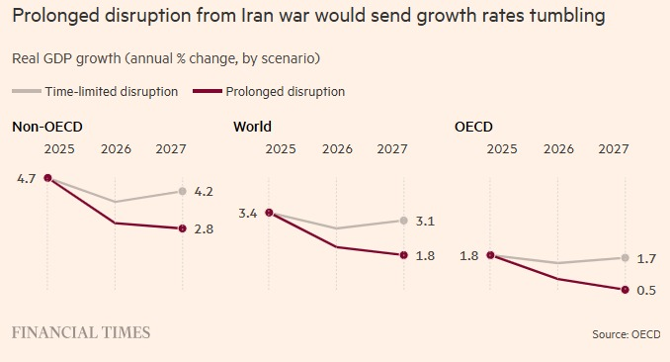

OECD itself warned on June 4 of a “dark scenario” for the global economy if the energy crisis drags on into the second half of 2027: global growth would collapse to just 2.1% this year and 1.8% next — levels last seen in the pandemic and the 2008 global financial meltdown. Energy prices would surge 50% above futures markets, triggering shortages, scarring effects on potential output, and severe hits to AI investment and semiconductor supply chains, the OECD warns. Central banks would be forced to hike interest rates by 0.5–0.75 points to fight inflation, squeezing governments’ already tight fiscal space further.

Oxford also highlighted uncertainty surrounding China’s inventory position, which is playing a major role. Between them, China and the US consume a third of global oil making them central to how the crisis plays out.

The IEA estimates that Chinese oil demand has fallen by only 0.1mbpd, far short of the fall in imports. Lower refinery runs and some switching from oil to coal in petrochemical production may explain part of the gap, but the scale of the adjustment remains difficult to reconcile.

Chinese imports fell by 3.6mbpd in April while observable inventories remained broadly unchanged, leading some analysts to suggest that the country may be drawing on underground reserves that are not visible through satellite monitoring. If those stocks prove more limited than expected, Chinese imports could rebound sharply, accelerating pressure on global supplies.

The US also remains a critical variable. US exports rose by 3.5mbpd in April, helping to ease shortages elsewhere, but any move by President Donald Trump to restrict exports in an effort to contain domestic fuel prices could tighten global markets further and hasten the depletion of inventories.

Follow us online