Iran war is Asia's Ukraine moment, rapid green energy rollout will accelerate

Three quarters of the world's population live in fossil importing countries and bleed out at least 3% of GDP every year to import oil to run their cars and power plants. However, the rollouts of green energy are so rapid and have become so cheap that just the new renewable green energy capacity built in 2025 could cut most countries' imports by 70% according to a new report by EMBER.

Net importers spent $1.7 trillion in 2024. If fuel prices rise, this number rises. For every $10 per barrel increase in oil prices, global net import costs rise by around $160bn per year, EMBER reports.

But clean energy offers a permanent solution.

By not only scaling “electrotech” – EVs, renewables and heat pumps – much of that fossil fuels use could be replaced in road transport, heating, and power. “It would enable importers to cut their fossil fuel imports by 70%.”

“The global fleet of electric vehicles avoided oil consumption equivalent to 70% of Iran’s exports in 2025. Global solar growth in 2025 alone could displace gas-fired electricity equivalent to all LNG exports through the Strait of Hormuz that year.”

Asia, which imports 40% of its oil through the Strait of Hormuz, is the most exposed. Asia is now facing the same reckoning Europe did in the 2022 energy crisis; 80% of the oil and 90% of the LNG that transits Hormuz was bound for Asian markets and has come to a stop.

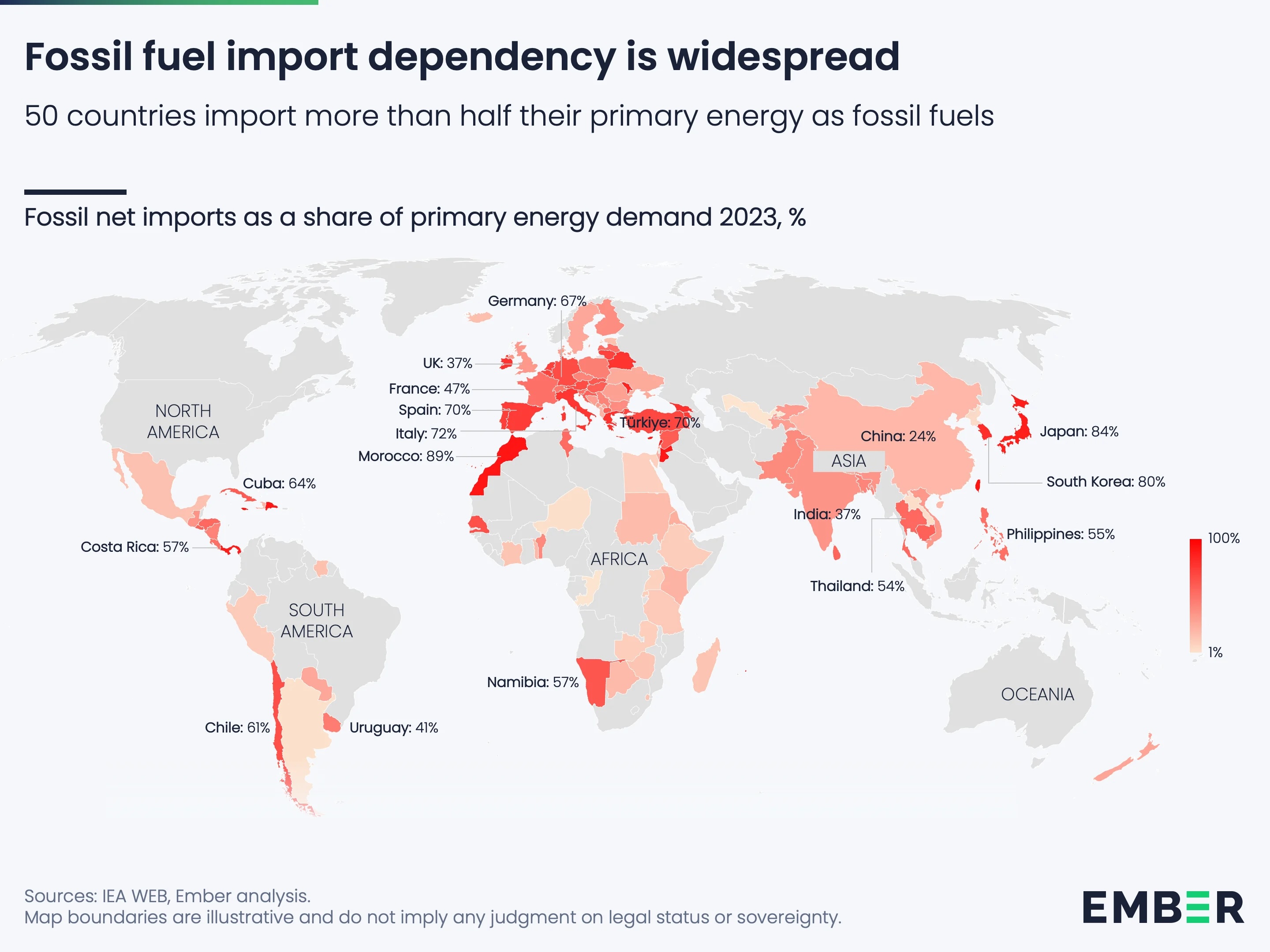

Fossil dependency is widespread

Three-quarters of the world’s population live in countries that are net importers of fossil fuels, according to analysis by Ember. Fifty countries import more than half of their primary energy in the form of fossil fuels, highlighting widespread dependence on external supply.

In Europe, Spain, Italy and Germany each import more than two-thirds of their energy needs. In Asia, reliance is even higher, with Japan and South Korea importing more than 80%. India imports 37%, while China imports about one-quarter of its energy.

The dependence leaves economies exposed when trade routes face disruption, particularly through key maritime chokepoints.

The financial cost is significant. Net fossil fuel importers spent $1.7tn on imports in 2024, reflecting the scale of global reliance on external energy sources.

Across 92 countries, representing two-fifths of the global population, net fossil fuel imports account for more than 3% of gross domestic product, underlining the economic burden associated with energy dependence.

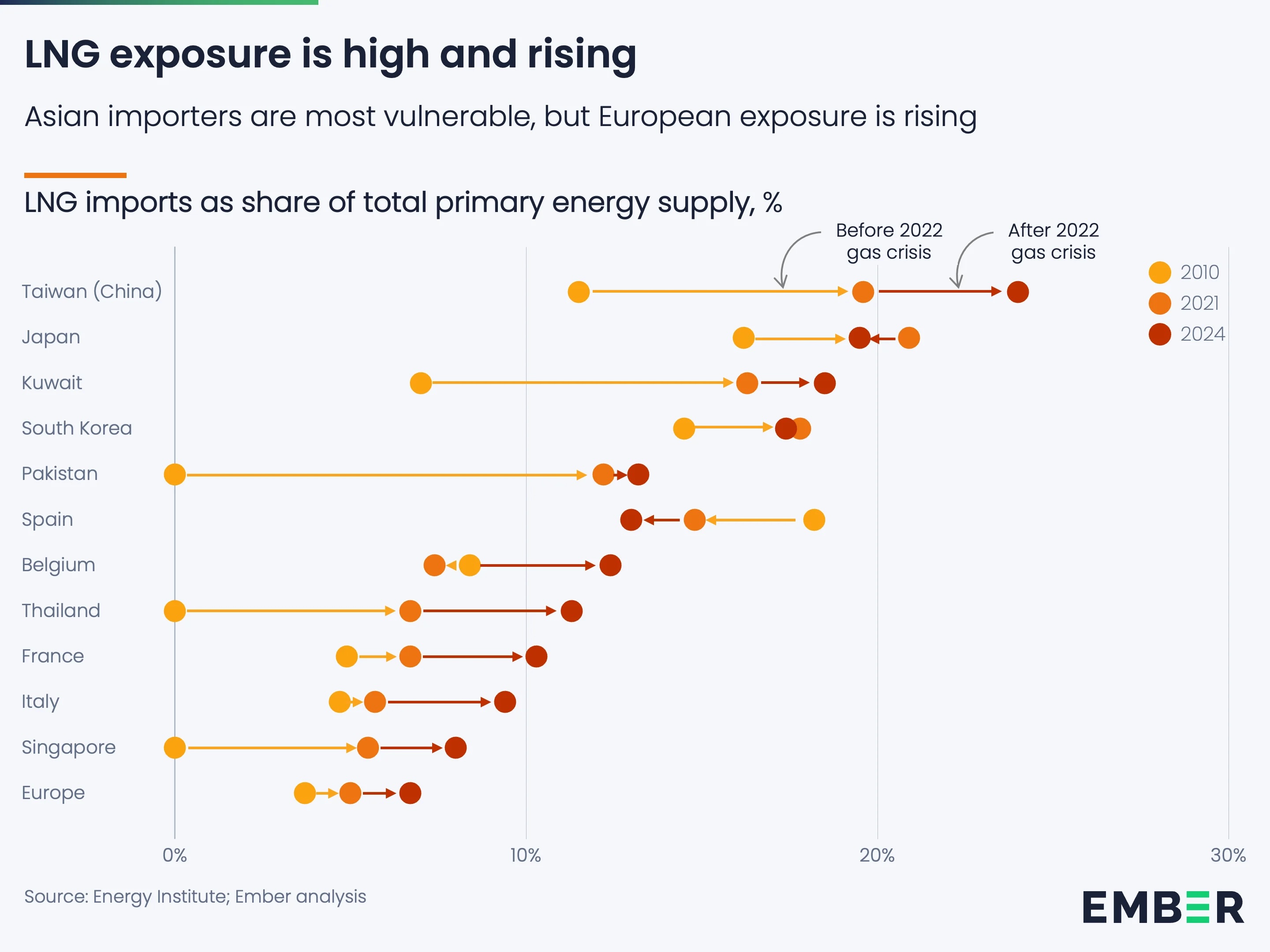

LNG dependency is rising

At a global level, liquefied natural gas from the Gulf plays a smaller role than its oil exports. Gulf LNG accounts for less than 1% of global primary energy supply, compared with 9% for Gulf oil.

Exposure to LNG imports has, however, been increasing. Around 60% of the world’s population live in countries that are net importers of LNG, reflecting growing reliance on seaborne gas supplies.

In at least nine countries, LNG imports account for more than 10% of total energy supply. Taiwan is the most exposed, with LNG making up 24% of its energy mix, followed by Japan at 20% and South Korea at 17%.

In several markets, dependence on LNG increased following the Ukraine crisis, as countries sought to replace pipeline gas with imported supplies, heightening vulnerability to disruptions in key shipping routes such as the Strait of Hormuz.

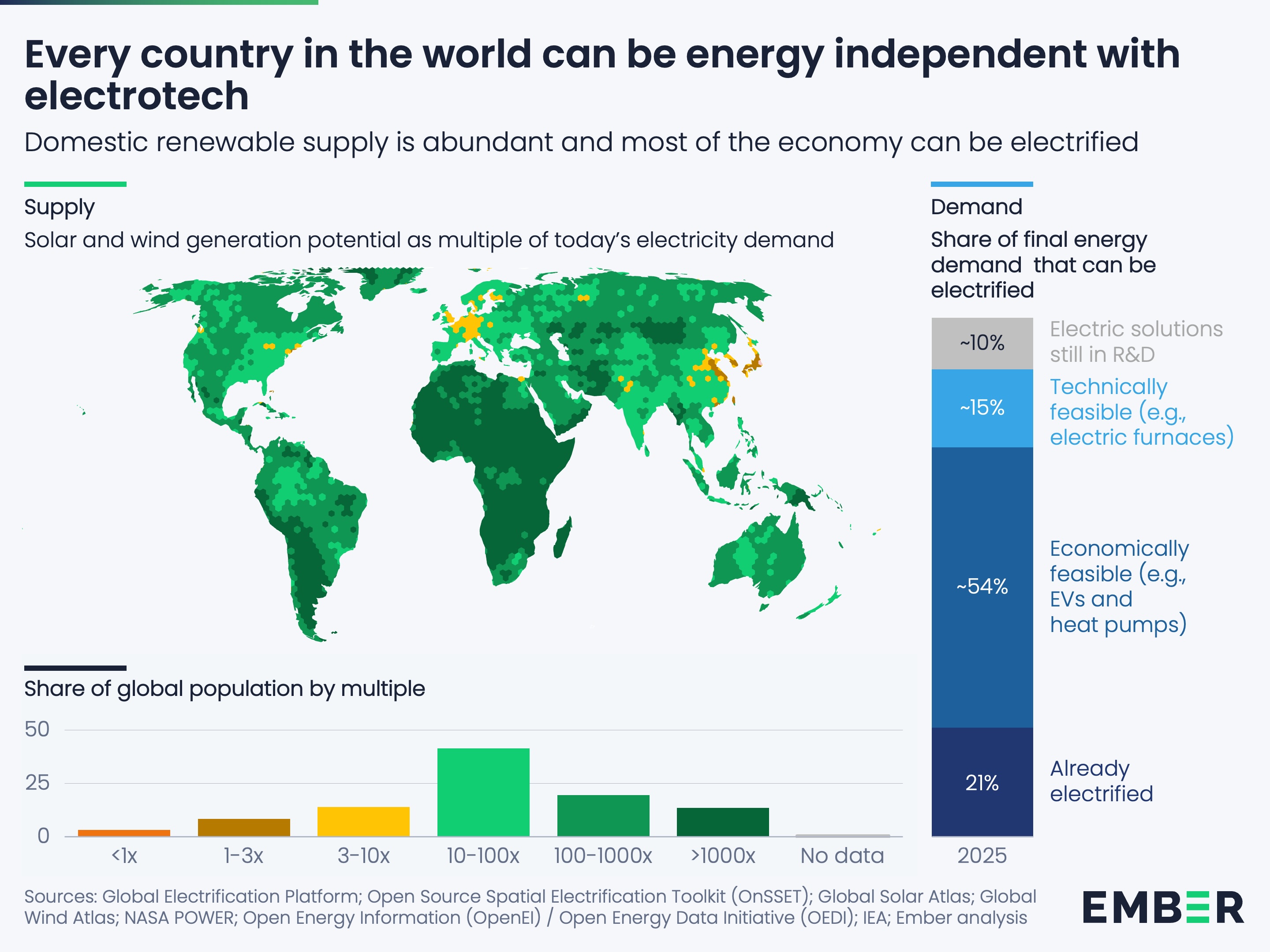

Eletrotech solution

Electrification technologies could enable countries to significantly reduce dependence on imported fossil fuels, with proven solutions already available at scale. More than three-quarters of the global economy can be electrified using existing technologies, while all countries have sufficient wind and solar resources to meet that demand domestically.

“Three levers do the bulk of the work. Solar and wind replace imported fossil-fuelled power generation. Electric vehicles replace imported oil in road transport. Heat pumps replace imported gas and oil in heating. If all three were scaled to replace imported fossil fuels in their respective sectors, importers could reduce their bill by around 70%.”

Electric vehicles are already price-competitive with internal combustion engine cars and widely available. Replacing imported oil used in road transport with EVs could cut import bills by more than one-third, equivalent to around $600bn a year.

Solar technology costs have declined sharply. Panel prices have halved since 2022, while annual installations have nearly tripled over the past four years. Battery prices have fallen by 36%, and annual deployment of grid-scale batteries has increased sevenfold. The combined cost of dispatchable solar power — including panels and storage — has fallen to $76 per megawatt hour for countries importing equipment without tariffs.

“The growth in global solar generation in 2025 alone could displace gas-fired electricity equal to all LNG exported through the Strait of Hormuz that year. In 2025, 82mn tonnes of LNG went through the strait; used in gas power plants that could generate about 600 TWh of electricity. The IEA calculated that global solar generation rose by more than 600 TWh in 2025.”

Beyond the immediate shock, this crisis will reshape energy markets in three ways:

Asia’s Ukraine moment: Russia’s invasion of Ukraine that began in 2022 galvanised Europe into action to reduce its dependency on Russian fossil fuels. Four years later, the US-Israel war with Iran will inspire Asia to reduce its dependency on imported oil and gas.

LNG demand growth in Asia is over: there is a battle between gas and solar for the future of electricity generation in Asia. At a stroke, this war has dramatically weakened the case for LNG.

Peak oil sooner: A decade ago, IEA saw no oil peak demand before 2050 at all. Then it forecasted the late 2030s, and then 2030. Its latest forecast put it at 2029, at around 106mn barrels per day (mbpd), not much above 2025 levels of 104 mbpd.

Follow us online