Latin America oils up as Hormuz crisis reshapes global energy supply

The conflict that has effectively closed the Strait of Hormuz, a conduit for one-fifth of global crude and a significant share of gas supplies, has done more than spike oil prices. It has laid bare how dangerously concentrated energy supply had become around a single chokepoint, sending importers scrambling for more reliable sources. Increasingly, they are looking to the Americas.

Latin America was already deep into a production surge before the first US-Israeli strikes on Iran on February 28. Now that expansion has acquired new strategic weight. Brazil, Guyana, Argentina and Venezuela together are projected to account for roughly 44% of global crude supply growth between 2025 and 2030, adding close to 2.5mn barrels per day out of an expected worldwide increase of 5.6mn bpd, according to Rystad Energy. The consultancy has described South America as "the world's most consequential source of incremental supply" at a moment when importers are actively seeking alternatives to Gulf barrels no longer able to move freely through the Hormuz chokepoint.

The region "does not replace the Middle East, but it meaningfully mitigates concentration risk by combining stable investment environments, visible project pipelines and scalable resource potential," Radhika Bansal, senior vice-president of oil and gas research at Rystad Energy, told Bloomberg’s Juan Pablo Spinetto. This positions Latin America as "one of the most important contributors to global oil supply growth over the coming decade."

The financial stakes have sharpened quickly. Rystad calculates that, at its revised 2026 Brent forecast of $89 a barrel — up from $60 in January — government revenues across South America will rise by roughly $43bn this year relative to the pre-war baseline. Petrobras, Brazil's state-controlled oil company, stands to capture the largest share: around $13.1bn in additional revenue against that original forecast.

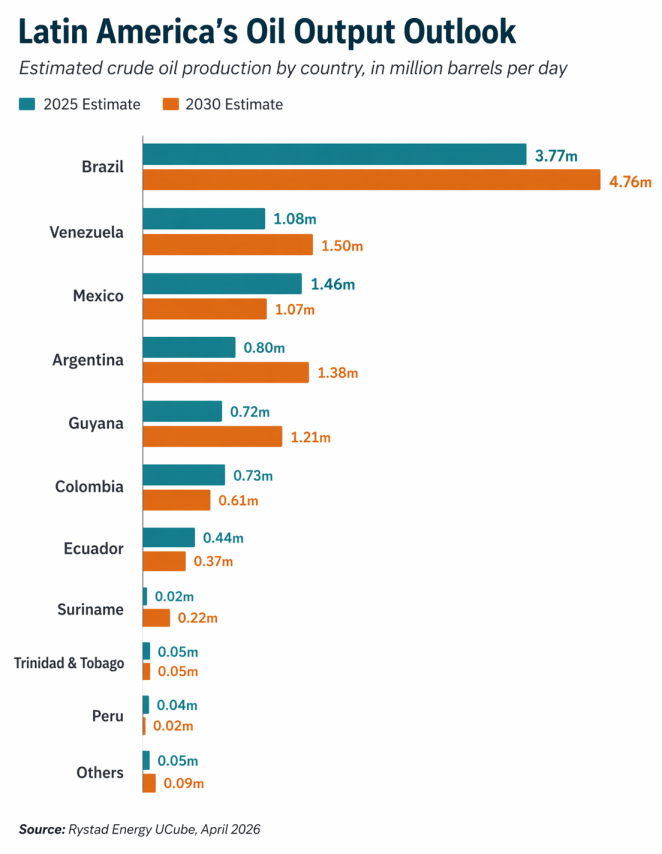

The producers: who gains and by how much

Brazil is the region's anchor story. Petrobras is targeting a place among the world's top five producers by 2030, driven by prolific presalt fields including Búzios in the Santos Basin. The company reported output of 5.3mn barrels of oil equivalent per day in February 2026, up 16% year on year. Together with Guyana, Brazil dominates the global market for floating production, storage and offloading vessels, both in active platforms and in the project pipeline.

Rystad estimates that accelerating offshore developments across Brazil, Guyana and Suriname could add more than 1mn boepd over the next decade, requiring around $33bn in incremental greenfield capital spending through 2035. In Guyana, ExxonMobil's Yellowtail project came online at an initial rate of 250,000 bpd, and the consultancy believes debottlenecking at the Errea Wittu, Jaguar and Hammerhead fields could unlock a further 80,000–90,000 bpd. The binding constraint is not geology or economics, Rystad warns, but shipyard capacity: the global order book for new FPSOs is already stretched thin.

Argentina's Vaca Muerta shale formation is the region's most dynamic near-term growth story. Output is running at around 600,000 bpd and is forecast to reach 1mn bpd by end-decade under a standard price strip, rising to 1.5mn bpd by 2035 and potentially 1.8mn bpd in a high-price scenario. At that level, the Vaca Muerta Oil Sur pipeline — still under construction — becomes the critical bottleneck. China is expected to emerge as the primary export destination, with consistent shipments beginning in 2027.

Analysts at Fitch Ratings, in a webinar earlier this month, noted that the oil shock is "only really great news for Argentina" among the region's net exporters. That is because it addresses a previously existing vulnerability: the country's need to rebuild foreign exchange reserves and stabilise its external accounts — a problem that the other net exporters, Brazil and Colombia, had largely resolved before the conflict began.

Colombia and Ecuador, the two smaller net exporters, gain a terms-of-trade benefit but face a difficult domestic balancing act. Ecuador has spent years unwinding fuel subsidies and risks social unrest if it allows domestic prices to jump sharply, while re-subsidising would undo fiscal gains made at considerable political cost. Fitch flagged similar tensions in Argentina, where the fiscal surplus is a central pillar of the current policy framework under President Javier Milei, and aggressive fuel subsidies could erode it.

Venezuela: the biggest prize, the longest odds

No country has attracted more attention from energy investors since the conflict began than Venezuela. It holds the world's largest proven oil reserves at more than 300bn barrels, and the ousting of Nicolás Maduro in January has opened the door to international oil companies after decades of resource nationalism, mismanagement and widespread corruption.

Under a $100-per-barrel scenario, Rystad estimates Venezuela could add 910,000 bpd by 2035, with more than half coming from existing fields in the East and West provinces where medium-grade crude costs just $7–$8 per barrel to produce. A new Hydrocarbon Law enacted in late January, spearheaded by acting president Delcy Rodríguez, restructures the terms for foreign investors, lowers the fiscal burden and, crucially for companies burned by Chávez-era nationalisations, provides access to international arbitration.

Commercial interest has moved swiftly. Shell signed preliminary agreements with state oil company PDVSA in early March covering offshore gas and onshore exploration. Trading houses Vitol and Trafigura have moved approximately 27mn barrels of Venezuelan crude since the post-Maduro licensing expansion. Chevron, which retained a presence throughout the Chavista years, now operates under an indefinite licence. ExxonMobil, whose chief executive Darren Woods had described Venezuela as "uninvestable" as recently as January, has since deployed technical teams to assess potential opportunities, in a striking reversal.

"In a new world where Middle Eastern oil exports decline or become unreliable, some companies that were hesitating until there is a return to democracy will now say it may be worth taking a risk," said Alejandro Werner, a former director of the IMF's Western Hemisphere department, according to the Miami Herald.

UBS, in a recent regional assessment, cautioned that Venezuela's recovery remains dependent on the oil sector but that the absence of a clear legal framework continues to dampen investor confidence. Neither the government nor Washington, it noted, appears to be prioritising debt restructuring for now.

Mexico: the awkward exception

Mexico fits uneasily into the regional recovery narrative. Once the dominant force in regional oil output, Mexico has seen production slide steadily as its ageing fields run down. Rystad forecasts national crude production will fall from 1.46mn bpd in 2025 to 1.07mn bpd by 2030 — the steepest projected decline among major regional producers and a stark contrast to the expansion elsewhere.

The nationalist energy policy of the ruling Morena party, which has consistently favoured the state oil company Pemex over private operators, has left Mexico poorly placed to capitalise on the current price environment. President Claudia Sheinbaum has mooted a greater willingness to admit private capital into the energy sector, but the impact on output has yet to materialise.

Fitch assessed the net fiscal impact on Mexico as roughly neutral: higher oil revenues for Pemex are largely offset by the cost of subsidising domestic fuel. UBS flagged that Moody's is likely to move Mexico's sovereign outlook this year, though investment-grade status itself is not seen as in question.

The macro picture

For the broader region, the oil shock is not a simple windfall. Fitch's cross-sector analysis found that of 36 Latin American corporate sectors assessed, nine face a credit threat under an adverse scenario, including airlines, chemicals and Brazilian agribusiness, where dependence on Middle Eastern fertiliser inputs adds to cost pressures. The consultancy noted that Iran accounts for roughly 25% of Brazil's corn export market, an additional vulnerability.

Brazil illustrates the tension most clearly. Its central bank had been on course to cut rates from 14.75% by year-end, but energy-driven inflation risks delaying that cycle. Brazilian corporates already carry the weakest interest coverage ratios among global peers, and for some issuers, interest payments are consuming 50–75 % of EBITDA, according to Fitch. Petrobras revenues benefit directly; the broader economy does not.

Capital Economics, in a note published this week, argued that the outlook for regional bond markets hinges on the Middle Eastern conflict's trajectory. If hostilities ease and energy prices fall, Latin American bonds are positioned to outperform across emerging markets as easing cycles in Brazil and Mexico resume. If the war drags on, bonds in parts of emerging Asia, with lower underlying inflation and stronger external buffers, are likely to prove more resilient.

UBS, drawing on conversations with regional policymakers, judged that Latin America was absorbing the shock "relatively well," citing a decade of improvements in fiscal frameworks and institutional credibility. It singled out Colombia as the most complex case in the region, facing higher inflation, political tensions between the government and its central bank, and an election cycle that makes fiscal adjustment difficult.

The longer game

The Iran conflict has compressed into months a strategic reorientation that was already taking shape over the years. The core argument for Latin American hydrocarbons has always rested on geology, proximity to Atlantic shipping lanes and, compared with the Gulf, a relative absence of interstate conflict. All three of those advantages look more compelling today than they did in January.

Writing in Bloomberg Opinion, Spinetto argued that the moment also calls for deeper regional energy integration: a natural gas corridor linking Argentina, Brazil and Chile; Mexico as a re-export hub for US gas; and long-discussed interconnections between Colombia, Central America and the Caribbean. Such infrastructure, he argued, could lift consumption, underpin manufacturing and expand exports — potentially transformative for a region that has historically left its energy endowment undermonetised.

"The pace of growth across South America will depend less on resource availability or economics and more on execution capacity, supply-chain constraints and the broader investment environment," said Rystad's Bansal. "Countries that provide clear fiscal and regulatory frameworks are better positioned to accelerate project sanctions and capture the upside from higher prices. Those that hesitate will simply watch the capital flow elsewhere."

Fitch raised a subtler long-term case: beyond the direct terms-of-trade effects, the conflict could generate a premium for regions distant from geopolitical flashpoints. Countries with large, underdeveloped resource bases — Venezuela and Argentina foremost among them — may attract investment that would previously have required democratic progress or legal certainty as a precondition, simply because the risk calculus has shifted.

The flow of capital into the region is accelerating. But Rystad's Bansal warned that the real constraint on South American supply growth is not geology or price: it is execution speed and regulatory consistency. With a ceasefire still fragile and prices liable to retrace sharply if hostilities in Iran ease, that window may be narrower than the current mood in Caracas, Buenos Aires and Rio suggests.

Follow us online