Latin America’s role in global supply set to increase because of Middle East war

But much of the boom may bypass Mexico

WHAT The Middle East war is focussing attention on more stable oil-producing regions such as Latin America

WHY Supply in the Middle East looks more unreliable

WHAT NEXT Mexico may miss out, because it imports so much hydrocarbons

A prolonged oil price near $100 a barrel could give South America a larger role in global supply than many market watchers expected, according to Rystad Energy.

In the consultancy’s analysis, the region could add as much as 2.1mn barrels per day (bpd) of extra crude output by the middle of the next decade, helped by deepwater projects in Brazil and shale growth in Argentina. That prospect has gained urgency after war in the Middle East sharpened fears about the world’s dependence on the Strait of Hormuz, a key route for oil and gas exports.

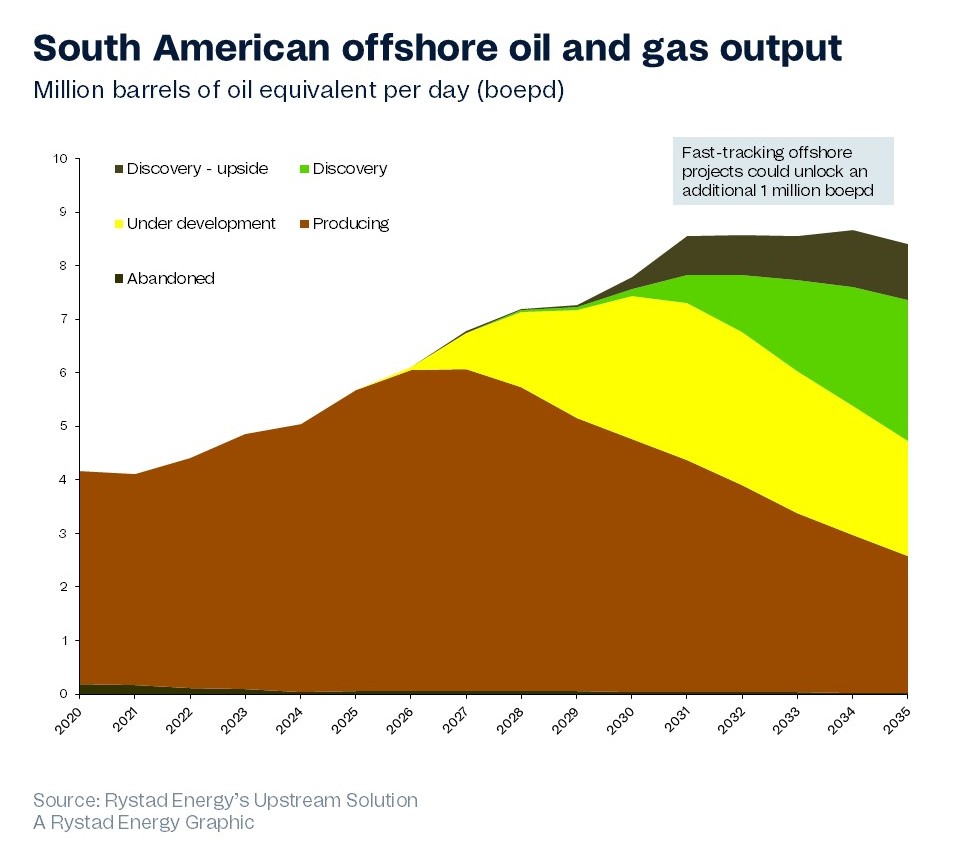

Rystad’s Radhika Bansal said the recent shock has exposed how concentrated global supply remains around one maritime chokepoint, while also drawing attention to South America as a major alternative source.

In her view, the region combines scale, strong geology and, in several countries, a more predictable political backdrop than many other emerging supply centres. The immediate upside is centred on offshore Brazil, Guyana and Suriname, where faster project development could lift output by more than 1mn barrels of oil equivalent per day over the next decade, backed by roughly $33bn in extra greenfield spending through 2035.

Brazil, the anchor

Brazil is expected to remain the anchor of that growth. Rystad says the country, together with Guyana, could account for a large share of the world’s next wave of floating production vessels, as operators push ahead with ultra-deepwater fields. For Brazil’s public finances, the higher oil-price environment is already meaningful: at current production levels, government revenue across South America is projected to rise by about $43bn this year versus a lower-price baseline, with Petrobras alone set to capture a large share of that increase. Rystad puts the Brazilian producer’s revenue gain at $13.1bn under its latest price forecast.

Guyana is a centrepiece

Guyana is another central piece of the story. ExxonMobil’s Yellowtail development is expected to reach a high initial output rate, and Rystad believes additional technical fixes could boost production at several nearby fields as well. Still, the consultancy says the bigger gains will come from bringing new projects to final investment decision sooner rather than simply squeezing more from existing assets. The main practical limit is not the rocks themselves but the industrial supply chain: there are only so many shipyards available to build the floating platforms needed for these developments.

Venezuela returns

Venezuela has also returned to investor discussions. Bloomberg’s Juan Pablo Spinetto notes that the country is back on the radar of major international oil companies after years of decline, though any sustained revival would depend on sanctions relief, reform and a more stable legal setting. Rystad estimates that, under a $100 oil scenario, Venezuela could add about 910,000 bpd by 2035, with a little more than half of that coming from existing fields in its eastern and western regions, where operating costs are low. Even so, the path forward remains uncertain. The article notes that some companies, including Shell and technical teams from ExxonMobil, have recently explored openings in the country, but the investment case remains highly conditional.

Vaca Muerta, a bright spot

Argentina’s Vaca Muerta shale basin is another bright spot. Rystad expects crude output there to keep climbing through the decade, with the possibility of reaching 1mn bpd by the end of the period and substantially more by 2035 under favourable assumptions. In a stronger price environment, the basin could go much higher, though pipeline capacity may eventually become the bottleneck. Exports from the region are likely to head increasingly toward China, which is expected to become a major destination once regular shipments are established.

Bloomberg’s Spinetto argues that the broader shift is not only about geology but also about geopolitics. Because conflict in the Middle East raises doubts about supply security, Latin America is being recast as a safer source of incremental barrels. That is attracting investor attention well beyond the oil patch. According to Bloomberg’s market reporting, Latin American currencies and bonds have held up better than many emerging-market peers since tensions escalated, aided by commodity exports and relatively high local yields.

Portfolio managers interviewed by Bloomberg said they have favoured the region because many of its sovereign and corporate issuers benefit from firmer energy prices or are less exposed to them. The market view is that the area’s oil exporters, particularly Brazil, Argentina and Colombia, stand to gain most from an environment in which prices remain elevated. Equities in the region have also outperformed broader emerging-market shares during the recent shock, helped by commodity exposure and carry appeal.

Mexico may miss boom

Still, not all countries are equally positioned to benefit. Mexico faces a more complicated picture. In reporting from Mexico Business News, rising oil prices are described as a mixed blessing: state producer Pemex may gain from stronger crude prices, but the country also imports large volumes of gasoline, diesel and natural gas, so higher oil costs quickly feed into consumer prices and industrial input costs. The Finance Ministry has said that each one-dollar rise in the annual average crude price adds roughly MXN10.7bn ($6mn) to federal petroleum revenue, but the same shift can also increase the cost of subsidies and fuel support.

Mexico’s fiscal exposure could become much larger if disruptions around the Strait of Hormuz persist. The Mexican Institute of Finance Executives has estimated that a prolonged crisis could create a revenue hit of more than MX$220bn, with the deficit moving toward 5% of GDP. The group said fuel subsidies are already expensive and would rise further if crude stayed near $100 a barrel. That would intensify pressure on public finances at a time when Mexico already depends on imported refined products and much of its natural gas.

The country’s structural energy challenges are also political. Platts reported that experts see Mexico as less likely than Brazil or Argentina to absorb a large wave of foreign investment because of regulatory uncertainty and a state-centred policy model. By contrast, countries that are willing to offer clearer rules, stronger partnerships and steadier fiscal terms are more likely to capture the current cycle of capital. That view was echoed by energy executives cited in the report, who argued that exploration and private collaboration will be necessary if the region is to turn higher prices into lasting production gains.

What next?

Taken together, the reports point to a common conclusion: the Middle East crisis has not only lifted prices, it has also reshaped the world’s search for reliable supply. South and Central America, with its offshore oil fields, shale basins and still-underdeveloped frontier prospects, is emerging as one of the clearest beneficiaries.

But the upside is uneven. Brazil, Guyana, Argentina and perhaps Venezuela may seize the moment if execution holds and investment keeps flowing. Mexico, despite its resource base, risks watching much of the boom pass it by.

Follow us online