LONG READ: Coal is back.

Coal is back. Having become a fuel for most of the last two decades, countries are scrambling to secure supplies of coal in the face of “ The largest supply disruption in the history,” according to the International Energy Agency (IEA).

While Europe has largely weaned itself off coal since it was the mainstay of the industrial revolution, coal continues to dominate SE Asia’s power mix, making up well over 40%-50% across the region, and remains important in the US as well.

Coal has long been more cost-competitive than gas and thanks to the legacy coal-fired power plants, it plays a parallel role with gas as utility companies and governments flit between the two fuels, depending on the vagrancies of the market price. However, since the start of Operation Epic Fury on February 28 and both a spike in the prices and evaporating supplies, countries are already switching back or at least building up their stocks in anticipation of worse to come.

The world needs to prepare for an extended energy shock, Michael Stoppard, principle of Stoppard Energy and formerly chief strategist on global gas at S&P Global, said in an op-ed in the Financial Times at the weekend.

Coal use will surge again like it did the last energy crisis in 2022, when coal use doubled. It remains the fallback marginal fuel in several systems. A lot of existing coal plants, though fewer, are still operational and unlike expanding renewables to building new nuclear power plants, these can simply be switched on again.

But the rebound in coal use this time round is likely to be less dramatic than in 2022. Nearly half of EU electricity is now renewables and the roll out of green energy in Asia, the biggest users of coal, has been dramatic. A recent report noted that when renewables first took off two decades ago it took a decade to increase generating capacity by 1GW. Last year that went down to half a day and the roll out is increasing at an exponential rate after wind and solar power became by far the cheapest sources of energy available to companies and governments. The Global South in particular, has embraced the green revolution, whereas in the Global North, while growing more slowly, renewables already represent a much larger share in their energy mix.

The rise in renewables will buffer many countries from the worst of an energy price shock. And also unlike 2022, when there was an unexpected economic growth bounce back, demand for power in Europe at least, is smaller thanks to a structural deindustrialisation caused by the very same 2022 energy crisis.

The 2026 energy shock has all the makings of a vintage crisis and could exceed that of 2022 that saw gas and power costs balloon ten-fold.

“Analyst estimates of disruption horizons are morphing from days to weeks to months. A two-month period of resumption is no longer the worst-case scenario, it is the best-case scenario,” Stoppard said. “Europe now needs to prepare for extended disruption, learning from the mistakes of the 2022 gas crisis.”

New playing field

Europe does not import much gas from the Middle East and Qatari LNG only accounts for some 12% of its gas imports, according to Eurostat. But as it was already in a gas crisis before the war in Iran broke out it is very price sensitive. Removing Qatar’s supplies from the market puts Europe into direct competition with Asia for the limited supplies of US LNG and prices were already the pre-2022 long-term average before the war in Iran started. Restarting coal-fired power stations is the obvious solution. In a coal report, the IEA predicts while demand was flat in 2025, it will now start to rise again.

“Global coal demand in 2025 is set to remain close to 2024 levels… is expected to rise by 0.5% to 8.85bn tonnes in 2026, a record high,” the IEA said. Coal has reached a “turning point” rather than a rapid decline, according to the IEA. One of the big changes is an anticipated explosion in demand for power thanks to the datacentre revolution, which was also not included in the 2015 Paris Agreement calculations. That will now be compounded by the dislocation of supply of fuel as a result of Operation Epic Fury.

Electricity demand remains central to the IEA’s outlook. “Two-thirds of global coal use today is for power generation,” and rising consumption, especially in the Global South. That will sustain coal demand despite rapid renewable expansion. Long-term, renewables are the desirable option, but coal’s appeal is the immediacy of its ability to quickly become an additional source of power in the midst of a fast-moving crisis.

Coal in Europe

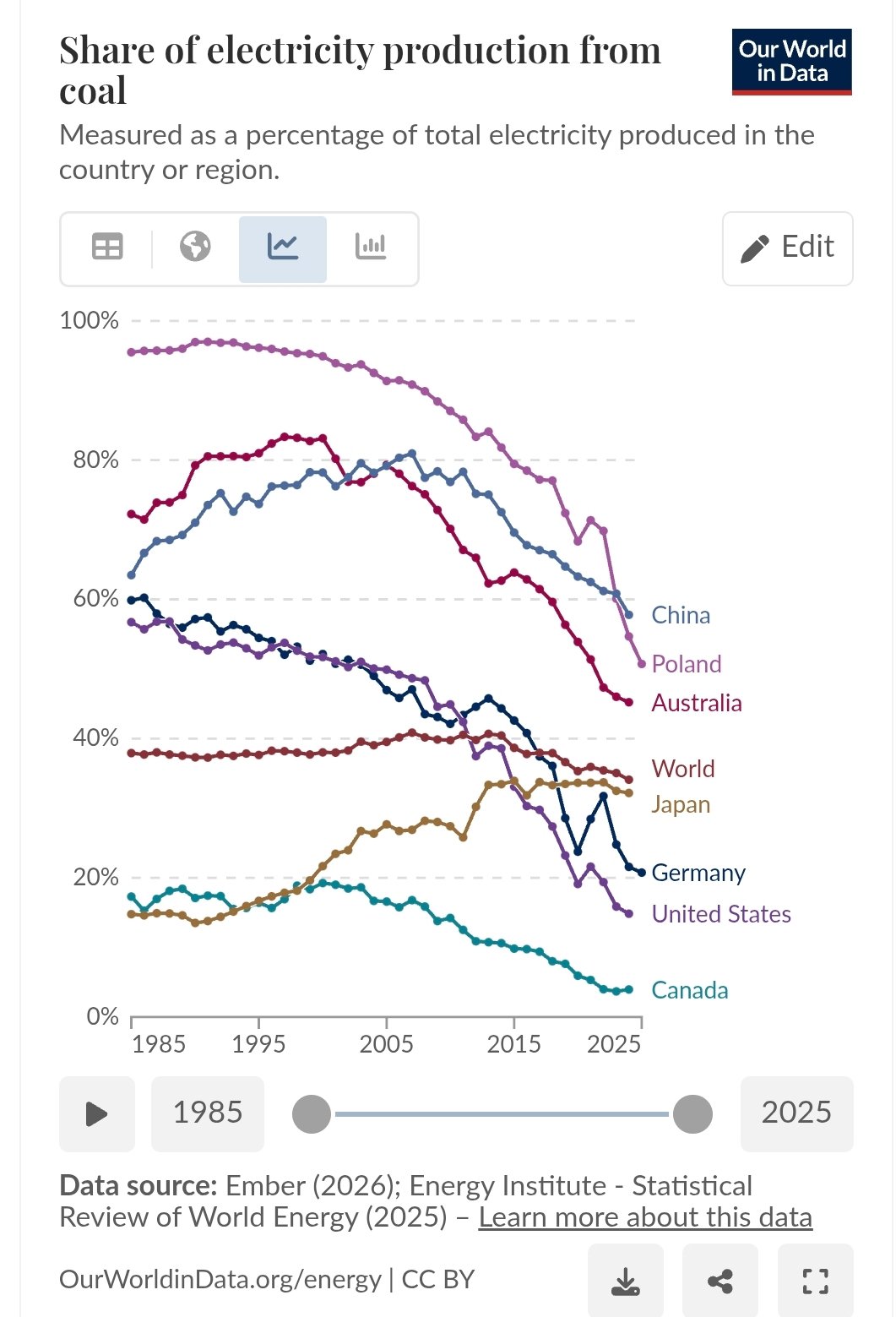

In 2021, coal was already in structural retreat across Europe due to climate policy, carbon pricing under the EU’s Emissions Trading System, and the rapid expansion of renewables. Coal accounted for roughly 15–16% of EU electricity generation. Gas remained the dominant marginal fuel.

The end of Russian gas supplies in 2022 triggered an unprecedented e nergy price shock and the revival for coal. Coal-fired generation increased by between 7% to 10% y/y that year. Germany, Poland, the Netherlands all reactivated mothballed coal plants that sent coal’s share in EU electricity generation to 18–20%.

By 2023, as the gas markets stabilised, thanks to the increase in LNG imports, the use of coal fell back again and by 2025, coal’s share dropped to roughly 10–12% of electricity generation, largely replaced by the expansion in renewables.

Natural gas and nuclear have both been popular alternatives but as the climate crisis accelerates the rollout of renewables has been both dramatic and rapid.

Today in Europe just under half of all electricity is generated from renewables and while enormous progress has been made in the last few years, green energy has not matured to the point where it can take over.

Europe has been a leader in adopting renewables and leaders like Norway now produce 83% of their power from wind and solar. However, until grid-level eight-hour batteries are rolled out that can cope with the “baseload problem” the revolution will not be complete.

Natural gas has always been seen as a stopgap solution and was supposed to be phasing out by now under the Paris Agreement projections. Now the mentality has changed, and gas is seen as a mitigator and its use is rising. The shutdown of Qatar's LNG exports has left a 20% hole in the market that the US and other producers cannot fill by themselves.

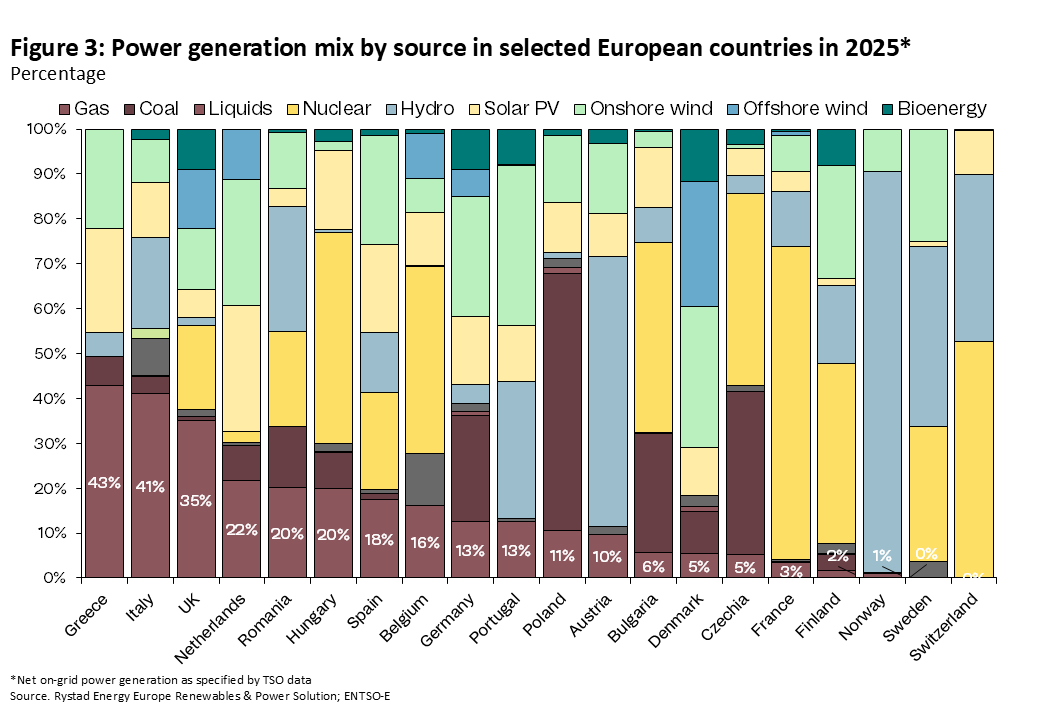

Thanks to its socialist legacy, Poland remains the most dependent on coal in Europe, which accounts for more than 50% of the power generated in 2025. Czechia is in second place, followed by Bulgaria and then Germany. Coal use amongst the remaining EU members remains relatively modest.

Gas use is widespread with Greece, Italy and the UK all depending on gas for at least a third of their power. Another eight countries rely on gas for between 10 and 20% of their power. Only the Nordic countries have reduced reliance on both coal and gas to almost nothing. Iran’s attack on the South Pars gas complex in Qatar on March 18 has now locked in a 17% in a long-term loss of production that will dramatically change the shape of the gas market.

Coal prices surge

Demand has pushed thermal coal prices up by about a fifth since the first US strikes on Iran two weeks ago, reaching roughly $146 per tonne, up 36% YTD and 60% y/y. The Asia-Pacific benchmark Newcastle futures are currently at their highest since the end of 2024.

For comparison, TTF gas prices were €60/MWh, up a massive 110% YTD, and almost double the pre-war €35/MWh average, as of March 22.

Thanks to the legacy coal infrastructure which hasn't all been decommissioned, coal and gas prices tend to move in parallel as the fuels can be swapped in times of crisis. Following Russia's invasion coal prices immediately doubled to more than $400 per tonne as utilities prepared for Russian gas supplies to be ended. After the Russian gas deliveries were cut off in 2022 the price of gas soared ten-fold to over €300/MWh.

With gas prices already rising from around €35MWh to more than €70/MTh as of March 22, that's already high enough to push utilities to switch to coal.

There is not as much coal capacity as there used to be after several large coal-fired power plants have been retired in recent years as part of the Green Deal. The UK closed its last coal plant in 2024, ending more than a century of coal-fired electricity in the birthplace of the industrial revolution.

Europe has also been actively closing coal plants, reducing the total coal-fired generation capacity by about 40%, according to reports. But those plants have only been mothballed. During the 2022 crisis Germany brought around a dozen plants out of retirement to make up for a gas shortage.

Coal in Asia

Asia remains the world’s biggest consumer of coal, consuming half of all coal burnt. But as part of its incomplete energy transformation it is heavily exposed to the war in Iran and also the world's largest consumer of gas. Asia used to buy more than 80% of Qatar's exports. Between them Japan, Singapore, Thailand, Taiwan, Pakistan and Bangladesh generate third or more of their electricity from natural gas.

Already looking into the abyss, governments across the region are now stocking up on coal, snapping up the remaining cargoes of coal on the water at record prices. Energy rationing measures are already being rolled out in Asia and the first government subsidized price caps.

What happens in China will be decisive for coal’s trajectory as it still generates half of its power using coal, says the IEA. “China consumes more coal than the rest of the world combined.”

Global trends are heavily dependent on China’s economic growth, policy direction and energy mix. Chinese demand is expected to decline slightly, but the IEA cautioned that stronger electricity demand or slower renewable integration “could turn the slight drop into a small increase”.

China is all of the world's largest coal producer, importer and consumer, despite its rapid rollout to become the global green energy champion. Coal use was supposed to peak in 2024, but it has failed to set out a coherent plan to phase out coal despite record growth in renewable energy and hitting its ambitious green energy targets. Nevertheless, China, the world’s biggest emitter of greenhouse gases (GHGs), saw its CO2 emissions go into reverse last year for the first time ever and well ahead of schedule.

Total wind and solar generation capacity has now overtaken coal, but that has also created a vast reserve of coal-fired generation capacity that protects it from the worst of the energy crisis. Today China uses less than half of its coal generation capacity and this number is dropping. If the energy crisis persists, Beijing can just restart its coal power plants – something that both China and Japan have already started to do.

Coal in SE Asia

India is even more dependent on coal than China. It generates 70-75% of its power using coal. It is also much less advanced in its transition to renewables, although that is now moving fast. Renewable energy is expected to account for 26% of India's total electricity generation by the end of this year when its wind and solar capacity will surpass that of Germany’s.

But India won’t hit the 50% of non-fossil fuel power generation for at least another five years. The IEA said in its report that “the most substantial growth in coal consumption between now and 2030 is expected to take place in India,”

In the Indo-Pacific region Indonesia is the main source of coal for most countries and remains the global export champion of thermal coal. Several Asian countries have already approached Jakarta to lay in supplies in anticipation of ballooning gas prices and the lack of supply.

SE Asia began to embrace LNG about 15 years ago. Thailand built two major import terminals and liberalized its market and so during the 2022 gas price shock the governments postponed the retirement of coal-fired units at the Mae Moh power plant, Bloomberg reports. This time around it's responding the same way and last week ordered its remaining coal-fired power plants to operate at full capacity.

Bangladesh is also heavily dependent on Qatari gas and has qualified as one of Tehran's friendly countries, granted a permits-for-passage to export oil via the Strait of Hormuz. Not to be caught with all its eggs in one basket, the authorities have also ordered the state-owned power stations to ramp up their use of coal since the start of the war in Iran.

Taiwan has long term energy supply contracts from the US but it's also preparing to restart the retired Hsinta coal-fired power plant, if supply disruptions persist, reports the Financial Times. Likewise South Korea is also preparing to boost its nuclear and coal-fired power generation

US big winner

The big winner from the fresh global gas crisis is the US which steps into the role of the premier LNG supplier for the global market. It has been rapidly expanding its gas production since the shale revolution took off in around 2008. However, LNG remains a relatively immature business. It's expanding rapidly and the US has several new projects in the pipeline that are due to come online over the next couple of years increasing the supply.

As reliance on gas has increased, the number of suppliers is dwindling making Asian countries in particular very nervous. The three big players in the LNG business were Qatar, the market leader, the US, the up-and-coming rival, and Russia, the home to vast deposits in the Arctic. Russia was taken largely out of the game by sanctions. Qatar has been removed, or at least reduced, by Operation Epic Fury. That leaves the US as the dominant player.

Asian buyers are extremely price sensitive but the geopolitical dimension of a narrowing market controlled by the US will also play a role, encouraging countries to keep some of their coal-fire capacity.

Trump is intending to capitalize on the gas chaos, which he sees as a bonanza for US companies. Trump is ramping up LNG production and has cancelled the moratorium on new LNG export terminal terminals imposed by the Biden administration on environmental grounds.

While the rest of the world has been trying to get rid of their coal-fired power plants, Trump has been doubling down on what he calls “beautiful clean coal.” The US just announced that the Terra Energy Center is pouring $1bn into a deal for a planned coal project in Alaska, Bloomberg reports – the first investment in new US coal power since 2013.

The US coal industry has been in decline as utilities turned to cheaper and cleaner sources of energy. However, in a reversal to the rest of the world Trump has pulled America out of the Paris agreement and gutted the EPA of its Obama-era "endangerment finding” – a scientific conclusion that is the legal basis for US climate regulations. Instead he is promoting fossil fuels as the central plank to his “energy dominance” policies.

Coal’s share in the US power energy mix has fallen from around half to 16% now, according to Bloomberg. Trump has been looking for quick fixes to meet the mushrooming datacentre demand for power. The rollout on renewables and nuclear is too slow to meet this demand leaving fossil fuels as the only quick fix.

With Climate Crisis-denier Lee Zeldin in charge of the EPA, Energy Secretary Chris Wright ordered six coal parts that were slated for retirement to remain in service this month. The power plants across the rural South and Ohio will get $175mn of government funding to retrofit and modernize. White House issued an executive order telling the Department of War to purchase power from the coal-fired facilities.

Follow us online