IntelliNews Lambda: Germany slipping into gas crisis, EU will struggle to restock this summer

Europe’s gas market has been pushed back into a vulnerable position after a cold winter drained storage to well below seasonal norms, setting up a difficult test for summer refilling.

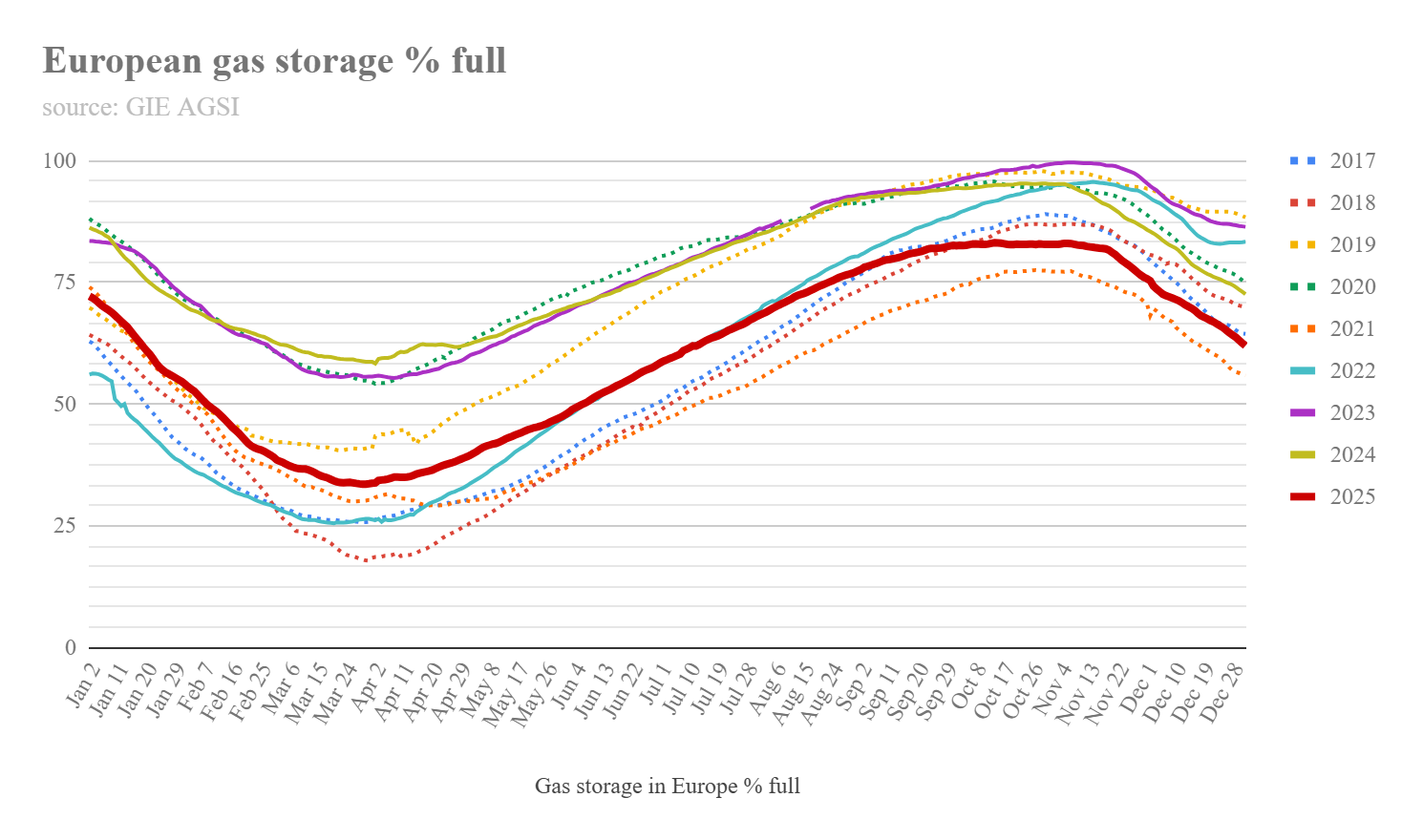

WHAT: EU gas storage is set to end the current heating season at around 20%, one of the weakest outcomes in 15 years, with inventories likely to recover to only about 70–75% by the start of next winter under average refill conditions. (chart)

WHY: An unusually cold winter, thinner starting inventories, and the loss of Russian pipeline flexibility have driven withdrawals far faster than normal, leaving Europe well below its historical seasonal trajectory.

WHAT NEXT: Europe will need an unusually strong summer injection cycle, supported by ample LNG supply and subdued Asian demand, to meet its regulated storage targets and avoid entering next winter with an uncomfortably small buffer.

Europe’s gas market has entered a more fragile phase after an unusually cold winter accelerated withdrawals over the past two months, dragging inventories far below what would normally be expected for this point in the year. Gas storage utilisation stood at just over 31% in the second half of February, compared with around 47% on a 15-year seasonal baseline once the crisis years of 2022 and 2023 are excluded. That gap of roughly 15–16 percentage points highlights how sharply this winter has deviated from historical norms and how thin Europe’s margin for error has become.

The speed of the drawdown has laid bare the system’s continued exposure to shocks, even as Brussels presses ahead with plans to phase out all remaining Russian pipeline gas and LNG within two years. While the policy direction is politically clear, it leaves Europe more dependent on LNG at a time when inventories are already running well below their normal seasonal trajectory.

Looking at the gas storage numbers from the perspective of deviations from the historical norms and the situation starts to look alarming. Standard deviations from the IntelliNews Lambda baseline of under two represent the norm and predictable supplies and prices, but deviations from two to four signal stress and beyond four standard deviations is the start of a crisis.

At EU level, the aggregate storage is around two to three standard deviations below seasonal norms, placing the bloc firmly in a stressed, though not crisis, regime. However, Germany is already in crisis territory with storage levels currently a bit less than five standard deviations below the baseline and drawdowns continue to be heavy.

The divergence highlights structural differences: Germany’s larger industrial base and heavier reliance on storage amplify its continued reliance on gas and vulnerability to weather-driven demand shocks. The wider EU benefits from geographic diversification and LNG inflows that cushion the impact of this year’s big freeze.

Cold snap comes after a weaker starting position

Europe entered the current heating season in a weaker position than the year before. EU-wide storage levels stood at about 83% at the start of winter, compared with roughly 95% at the same point a year earlier. That deterioration partly reflected the easing of storage regulations last year, which reduced some of the distortions that had driven summer prices sharply higher in previous seasons, but also meant the system went into winter with a thinner buffer.

Weather has been the dominant driver of the current situation. Prolonged cold, particularly across eastern Europe, pushed withdrawals well above seasonal norms through January and February. The divergence from historical patterns is stark in the data. In early February, storage utilisation fell to around 38%, versus roughly 55% on the long-run seasonal curve derived from a Fourier fit to the past 15 years excluding the crisis period. By February 20, inventories had slipped further to around 31%, while the baseline still pointed to the mid-40s.

The depletion has not been evenly distributed. Facilities in Germany, Europe’s largest gas market, have fallen to the low-20% range, amplifying concerns about late-season vulnerability if cold conditions persist. At the same time, Russia has stepped up attacks on Ukrainian energy infrastructure this winter, including assets linked to domestic gas production that normally meets the bulk of Ukraine’s demand. As a result, Poland has redirected additional gas flows eastward, with cross-border capacity set to rise from 15.3 mcm per day to 18.4 mcm per day from April.

Despite the strain, the situation remains far removed from the acute crisis conditions of 2022. Storage levels are the lowest for this point in the year since that period, but prices are far more subdued, with front-month TTF contracts trading in the €30–35/MWh range, reflecting a market that is tight but still functioning.

How Europe will end the heating season

The more important issue now is how Europe exits the heating season. A Fourier-based seasonal model of storage utilisation indicates that inventories typically continue to decline into late March or early April before reaching their annual low. Applying that seasonal profile to current conditions implies that EU gas storage will end the 2025–26 heating season at around 20%, placing the trough in the high-teens to low-20s. Such an outcome would rank among the weakest end-winter storage levels recorded in non-crisis years over the past 15 years.

That low exit point sharply raises the stakes for the summer refill season. Under average conditions, the same Fourier model implies that storage levels typically recover by around 50–55 percentage points between early April and early November. Starting from roughly 20%, that trajectory points to EU storage reaching only around 70-75% at the start of the next withdrawal season if refilling proceeds at a normal pace.

Reaching 90% by early November would therefore require a materially faster-than-normal injection cycle, exceeding the long-run average implied by historical seasonal patterns. Even an outcome in the low-to-mid-80% range would represent a strong refill performance relative to the non-crisis record, leaving limited tolerance for supply disruptions, stronger-than-expected LNG demand from Asia, or weather-driven increases in summer gas burn.

Forward markets have yet to fully reflect that challenge. The summer-winter spread remains narrow, offering limited commercial incentive to inject gas aggressively for storage. As a result, refilling may rely more heavily on compliance buying and risk management rather than market-driven arbitrage, at a time when physical constraints such as maintenance schedules, infrastructure limits and global LNG competition remain in place.

The EU may of course make further policy interventions to spur higher storage refill rates during the summer, though this in turn would drive prices higher, creating further market distortions.

Much will depend on how quickly new LNG supply ramps up and on demand trends in Asia, particularly China. While additional LNG volumes are expected to enter the market over the next two years, delays to major projects and uncertainty around ramp-up timelines mean Europe cannot assume a smooth supply response. Any rebound in Asian LNG demand would further tighten the balance just as Europe needs to accelerate injections.

Structurally weaker

Structurally, Europe’s gas system is weaker than it was before the war in Ukraine. The loss of Russian pipeline gas has removed a key swing supply, while widespread coal plant closures have eliminated another stabilising mechanism during periods of high prices. Inventories now carry a greater share of the burden of balancing the system.

On current trends, Europe should be able to make it through the remainder of winter without an immediate supply crisis. The greater test will come after the heating season ends. With storage likely to bottom out at around 20%, Europe faces a summer in which meeting the highest regulated targets for next winter will require an unusually strong refill performance, leaving the market more exposed to volatility than in the years immediately preceding the energy crisis.

Follow us online