Iraq’s US‑led energy realignment shapes production, exports and power

Iraq is deepening ties with US energy firms to reshape crude output, export routes and electricity supply, concentrating influence over future incremental barrels and grid resilience.

WHAT: Baghdad is inviting Chevron, Halliburton, GE and KBR into core fields, pipelines and power networks to anchor its next phase of energy development.

WHY: Fiscal strain, OPEC+ constraints and fragile infrastructure are pushing Iraq towards integrated partnerships that share risk while accelerating capacity, gas utilisation and grid stability.

WHAT NEXT: Future Iraqi supply, routing choices and geopolitical leverage will increasingly reflect how US‑linked projects shape incremental barrels and power reliability.

Iraq’s latest approvals for major US-led energy projects signal a deliberate effort to re-anchor its upstream growth, export strategy and power-sector stabilisation around American technical and financial participation, with potentially meaningful implications for future production control and regional geopolitics.

The emerging pattern points to Iraq using US firms not only as project contractors, but as structuring partners for a new phase of capacity expansion and market re‑engagement.

Energy engagement

The Iraqi cabinet has endorsed a cluster of energy and infrastructure agreements with leading US companies, framing them as part of a broader strategy to consolidate Iraq’s position among the world’s main oil exporters while addressing chronic power shortages.

Recent approvals cover upstream oilfield development, strategic pipeline design, power grid stabilisation and multimodal export corridors, tying hydrocarbons, electricity and transport planning together in a way that has rarely been achieved since 2003.

At the core are framework and technical cooperation arrangements with Chevron, Halliburton, GE and KBR, backed by explicit political messaging from Oil Minister Bassem Mohammed Khudair Al‑Abadi and provincial authorities in Basra that Iraq is offering a more predictable, secure and commercially attractive environment for international investors. For board‑level decision makers, the combination of upstream access, midstream advisory roles and power‑sector contracts suggests a more integrated route into Iraq’s energy value chain than has typically been available to single operators.

Upstream opening

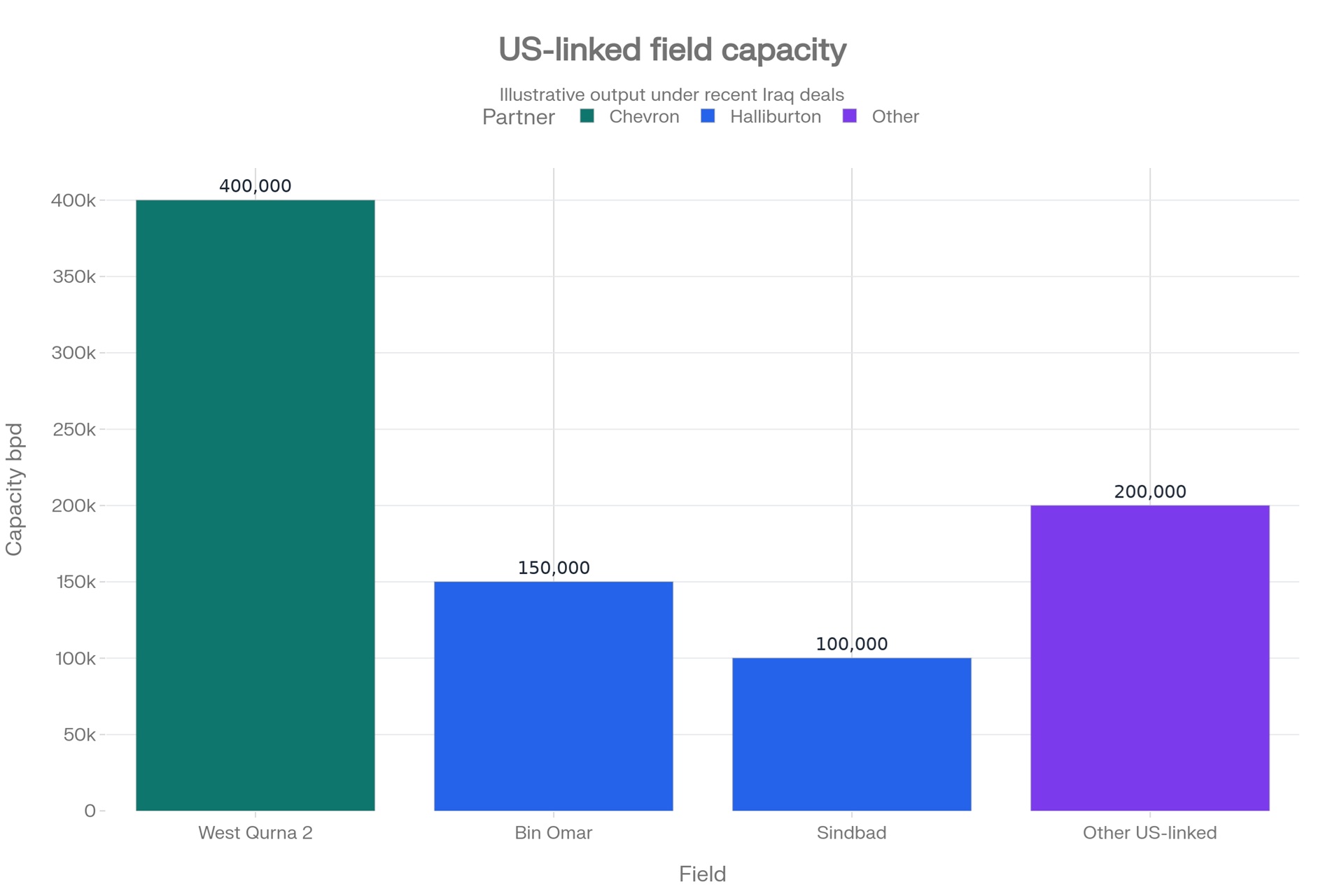

Basra Oil Co. (BOC) has signed a confidentiality agreement with Chevron to enable comprehensive technical data exchange on the giant West Qurna 2 oilfield, following the withdrawal of Russia’s Lukoil from development operations.

The arrangement is framed as a precursor to potential investment, giving Chevron the ability to evaluate reservoir performance, redevelopment options and incremental capacity from one of Iraq’s largest producing assets.

Al‑Abadi has described West Qurna 2 as a cornerstone of Iraq’s ambitions to raise production capacity, and has linked the Chevron engagement explicitly to a wider effort to “provide broad opportunities” for international companies under an “attractive and secure” investment regime.

From a governance perspective, the minister has been careful to emphasise that international operators are regarded as partners rather than mere service providers, with commitments to safeguard their interests while drawing domestic supply chains and local employment into project delivery.

Beyond West Qurna 2, the ministry has signalled it is exploring further investment opportunities with Chevron, suggesting that the confidentiality agreement may be the first step in a portfolio of upstream positions.

Capacity gains

In parallel, Iraq’s Ministry of Oil has signed a five‑year integrated management contract with Halliburton covering the Bin Omar and Sindbad oilfields in Basra. Under this agreement, Basra Oil Company and Halliburton will work to raise crude output at Bin Omar to around 150,000 barrels per day, while lifting associated gas utilisation to roughly 300mn cubic feet per day.

At Sindbad, crude production is targeted in the 80,000‑100,000 bpd range, with associated gas utilisation rising from 240mn to about 260mn cubic feet per day.

These are modest volumes in global terms, but they matter operationally: incremental crude capacity and higher associated gas capture translate into greater flexibility for Iraq’s power generation sector, cutting reliance on imported fuels and improving grid resilience.

Al‑Abadi has framed the deals as integral to Iraq’s strategy to expand capacity “in cooperation with international energy companies”, underscoring a preference for structured partnerships rather than purely state‑run development. Halliburton’s long‑standing presence in Iraq since 2003 is highlighted by the minister as a marker of continuity and operational familiarity, which helps to mitigate execution risk for new integrated contracts.

Strategic positioning

Beyond upstream operations, Iraq has moved to fast‑track direct co-operation with KBR for consulting services on the Basra‑Haditha crude pipeline – a flagship project intended to connect southern production with northern and western routes.

According to local media outlet Shafaq News, the Basra governor, Asaad al‑Eidani, has separately signed a memorandum of understanding with KBR covering wider provincial development, including redevelopment of Basra International Airport, rehabilitation of the Shatt al‑Arab waterway and support for the Grand Faw Port.

KBR President Jay Ibrahim said on LinkedIn that the initiatives are part of a broader effort to “advance strategic development projects” in Basra, while US Embassy Charge d’Affairs Joshua Harris has framed Washington’s support as deepening economic partnership with Iraq.

The coupling of energy infrastructure advisory work with transport and port development suggests that Basra is being positioned as a multi‑modal hub, with US firms embedded not just in upstream consulting but in the physical architecture of Iraq’s export strategy. This raises the prospect of US companies exerting influence over routing decisions and capacity build‑out, even where they are not the ultimate asset owners.

GE and the power pivot

On the power side, Iraq’s Ministry of Electricity plans to partner with GE on a comprehensive programme to upgrade and secure the country’s generation and transmission networks. The initiative is being presented as a system‑wide response to chronic outages, grid instability and fuel supply constraints, with GE’s role encompassing both hardware provision and network planning.

This dovetails with the Halliburton‑backed push to increase associated gas utilisation at Bin Omar and Sindbad, which aims to provide more domestic fuel for power plants. The combined effect, if realised, would be to intertwine US participation across the gas‑to‑power chain – from field‑level gas capture through to grid reinforcement – with clear implications for the operational resilience of Iraq’s electricity system and, by extension, industrial output. Board‑level decisions on engagement will need to weigh the potential upside against exposure to regulatory change and intermittently contested subsidy regimes.

Geography of influence

Perhaps the most geopolitically sensitive element of the recent approvals is the consortium formed by Chevron, Capital TI (US) and UCC (Qatar) to study new crude export routes from Basra via Haditha, with branches to Kirkuk–Ceyhan in Turkey and to Baniyas in Syria.

The studies will assess technical and financial feasibility for corridors that could diversify Iraq’s export options beyond the Gulf, reducing reliance on southern terminals and adding redundancy into the system.

The Basra‑Haditha‑Kirkuk‑Ceyhan route would reinforce connections to the Mediterranean through Turkey, while the Basra‑Haditha‑Banias line would provide a western outlet through Syria.

For US‑linked companies, involvement at the feasibility and design stage offers an opportunity to shape specifications, capacity assumptions and phasing, which in turn affect how much future production can be directed through assets they help configure.

In a context where Iraq has recently scaled back some headline capacity targets but continues to discuss expansions with OPEC partners, control over routing and offtake flexibility may become as important as nominal nameplate capacity.

Production outlook

Recent shipping disruptions in the Gulf left more than 8.3mn barrels of Iraqi crude stranded aboard tankers, contributing to a wider regional backlog that S&P Global Commodity Insights estimates at over 100mn barrels of crude and refined products.

Of that accumulated volume, around 90.5mn barrels were crude oil, with some 90mn barrels still awaiting shipment at the time of reporting; Iraq’s stranded volumes ranked behind Iran, Saudi Arabia and the UAE, but ahead of Kuwait, Qatar and Oman.

From an operational standpoint, this underscores the importance of both diversified export routes and more flexible production management. As Iraq and Oman have emerged as key contributors to the recovery in Middle Eastern oil exports, the gradual release of stranded barrels has provided temporary relief to global supply, with most cargoes destined for East Asian markets and exerting a moderating influence on prices.

However, analysts caution that the impact may be fleeting until output and refining capacity across the Gulf stabilise, highlighting continued vulnerability in regional logistics chains.

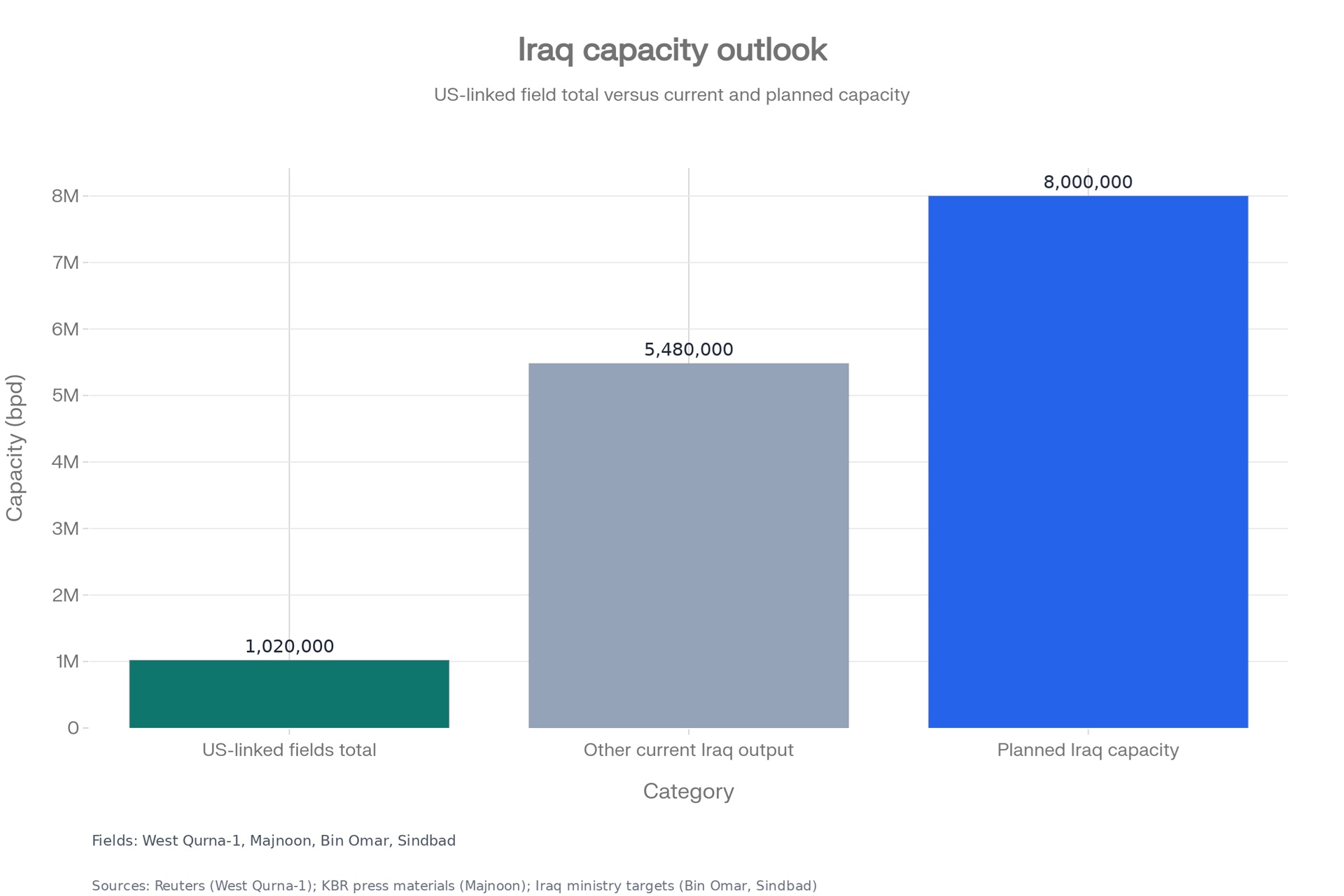

Within this broader context, the set of Iraqi fields where US firms now have, or are seeking, operational roles – notably West Qurna 2 (Chevron), Bin Omar (Halliburton) and Sindbad (Halliburton), alongside advisory positions on strategic pipelines – collectively represent a material, if still partial, slice of Iraq’s current and prospective production base.

Using illustrative capacity estimates drawn from recent ministry targets and commentary, these assets and associated positions suggest that US‑linked companies could influence a significant fraction of Iraq’s incremental capacity growth even if they do not operate a majority of total output.

Policy signalling

Al‑Abadi has repeatedly stressed that Iraq is committed to safeguarding the interests of international companies and creating employment opportunities and infrastructure improvements through social benefit programmes linked to investment projects.

This rhetoric aligns with ongoing discussions around reforms to the hydrocarbons framework, including proposed changes to the federal oil law and adjustments to production capacity targets that have occasionally sparked tensions with the Kurdistan Regional Government.

In summary, three themes stand out. First, Iraq is clearly positioning US firms as preferred partners in both upstream and midstream projects, signalling that long‑term relationships and technical depth carry weight in allocation decisions.

Second, the focus on associated gas and power‑sector stabilisation indicates that projects are being evaluated not just on oil output, but on their contribution to wider energy security – which can offer diversified revenue streams but also exposes investors to policy debates over domestic supply priorities.

Third, the geopolitical sensitivity of new export routes through Turkey and Syria, combined with episodic Gulf shipping disruptions, adds a layer of risk that boardrooms will need to manage through scenario planning and contractual protections.

In practical terms, the new wave of agreements suggests that executives seeking exposure to Iraq’s next phase of growth will increasingly have to think in system terms: fields, pipelines, ports and power grids as an integrated portfolio rather than discrete projects.

Follow us online